An eviction definitely causes a critical financial and legal paper trail for a renter. This trail further creates significant barriers in securing housing in the future, obtaining favorable credit terms, and achieving financial stability.

So, if you are a renter, you need to understand the mechanics of how an eviction is recorded, where it appears, and how long does an eviction stay on your record is crucial.

The general rule of thumb is that an eviction will remain on your record for seven years. However, this answer does not give a clear picture of the reality.

The type of record generated, the involvement of debt collectors, and many other factors determine the timeline.

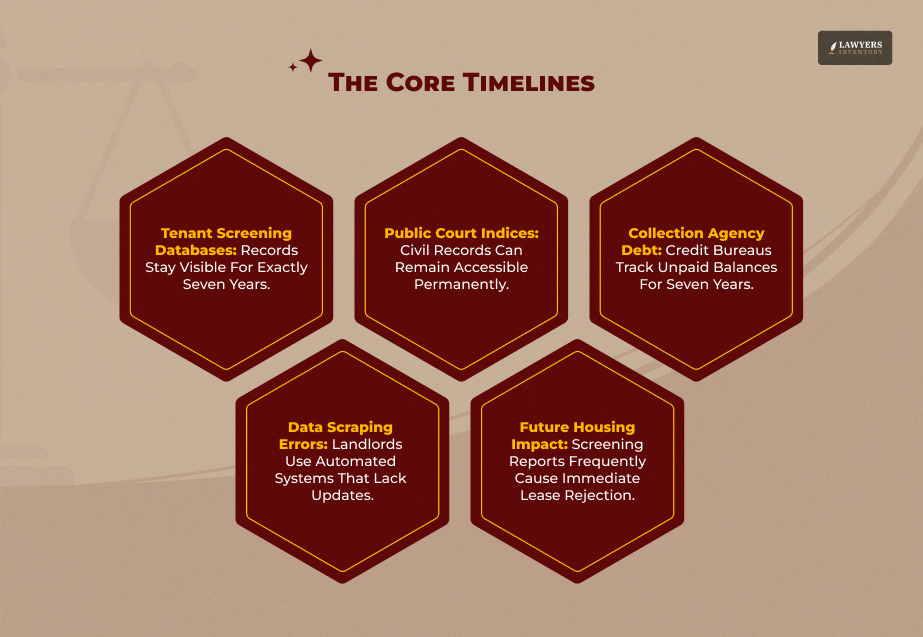

How Long Does An Eviction Stay On Your Record? The Core Timelines

When you are assessing how long an eviction stays on your record, you have to separate the event into the three following distinct financial and legal categories.

- Tenant Screening Reports

- Civil Court Records

- Credit Bureau Histories

Each area operates under different regulations and maintains its own timeline.

1. Tenant Screening Databases (7 Years)

“The Act (Title VI of the Consumer Credit Protection Act) protects information collected by consumer reporting agencies such as credit bureaus, medical information companies and tenant screening services. Information in a consumer report cannot be provided to anyone who does not have a purpose specified in the Act.” – Fair Credit Reporting Act (Source: Federal Trade Commission)

However, many landlords, complying with the specific purpose, often rely on the specialized tenant screening companies such as TurboTenant, AppFolio, or TransUnion SmartMove before getting renters on board.

The Fair Credit Reporting Act (15 U.S.C. § 1681c(a)(2)) also mentions that consumer reporting agencies and tenant screening companies cannot report adverse public record information, including eviction filings and judgments, which are older than 7 years.

Also, this span of seven years starts on the exact date the eviction lawsuit was filed in court. It is not the date when the judge gave the ruling or when the tenant had to move out.

Once the seven years are over, the tenant screening databases need to drop the records automatically.

Understanding The Ecosystem Of Consumer Tracking

If you want a removal of your eviction record, you have to understand where the data is stored.

With information getting fragmented across many networks, an eviction record can disappear from one platform and yet be very much visible on another.

Specialized Screening Agencies

We are all well aware of our credit scores. However, very few people know that they also have a rental history score managed by specialty consumer reporting bureaus.

Some prominent companies operating in this area are:

- Contemporary Information Corp. (CIC)

- CoreLogic Rental Property Solutions

- RealPage (LeasingDesk)

- Experian RentBureau

Now, what do these companies do? Their core activities include the following:

- Aggregating Tenant Data

- Tracking Previous Addresses

- Lease Violations

- Timely Rent Payments

- Legal Filings

Suppose you are a tenant and you are applying for a new apartment. Now, the landlord will aggregate tenant data, track previous addresses, and check lease violations, timely rent payments, and legal filings.

The landlords will pay for any of the previously mentioned farms for the background check. Now, if an eviction filing matches the applicant’s name and Social Security number, the application is frequently flagged for automatic rejection.

The Problem Of Data Scraping And Record “Echoes”

Suppose a tenant resolves an eviction successfully. Still, the data inaccuracies will run rampant through automated tracking systems.

Screening companies usually use automated bots to scrape court dockets.

Now, there are instances where a landlord has filed a case, and the case is dismissed later.

However, the screening company might only scrape the initial filing and fail to update its database with the dismissal.

So, the record remains inaccurate, unfair, and damaging for the tenants. The erroneous record is gone only when the tenant manually disputes the error.

2. Public Civil Court Records (Indefinite/Permanent)

An eviction is fundamentally a lawsuit, and in legal terms, an eviction is an unlawful detainer action.

In simple words, when a landlord files an eviction lawsuit, there is a civil court case.

Now, county and municipal records are not bound by the FCRA. In fact, they are governed by the state public record laws.

So, the specific law of a state will determine how long an eviction stays on your record.

After seven years, the eviction record will disappear from a private tenant screening report. However, the case remains searchable in the public court index immediately.

Anyone who goes directly to the local court portal or county clerk’s office can find the record of the lawsuit, regardless of how much time has passed.

Also, as I have mentioned, the span will depend on the state law. For example, in Illinois, the span is 3 years, and in New York, it is 20 years.

3. Credit Reports And Collection Accounts (7 Years)

Many tenants think that eviction shows up on a standard credit report platform such as Equifax, Experian, or TransUnion.

However, the reality is these platforms never show eviction, civil lawsuits, or initial unlawful detainer judgments.

Having said that, if the eviction is happening because you failed to pay the rent, you have caused any damage to the property, or any legal cost is involved, the landlord can turn this outstanding balance over to a third-party collection agency.

This third-party agency will again report the collection account to the credit bureaus. Then, these credit bureaus will follow the FCRA and keep the eviction report for 7 years and 180 days from the original date of delinquency.

Thus, it will impact your credit score, making it difficult to qualify for credit cards, auto loans, or competitive mortgage rates.

What Are The Financial And Personal Impacts Of Having An Eviction Record?

Having an eviction record will impact more than the effect of your background check. It creates a cascading sequence of financial and personal hardships that can trap individuals in a cycle of housing instability.

The “Blacklist” Effect And Substandard Housing

When the agencies scrape an eviction record, the effect is that the housing market will shrink for you immediately.

Professionally managed and big apartment complexes have strict policies, and they will reject any applicant with an eviction filing on their record within the past seven years.

So, the tenants will have to pick among the “alternatives.”

The Premium On Risk: Sky-High Security Deposits

A landlord may agree to overlook an eviction record with a very high upfront cost. Sometimes this means paying a security deposit, which is double or triple the standard rate.

Furthermore, they can ask you for a deposit for the first month, last month, and a security deposit all upfront.

They even need a qualified guarantor or co-signer, earning four to five times the monthly rent and agreeing to take on full financial liability for the lease.

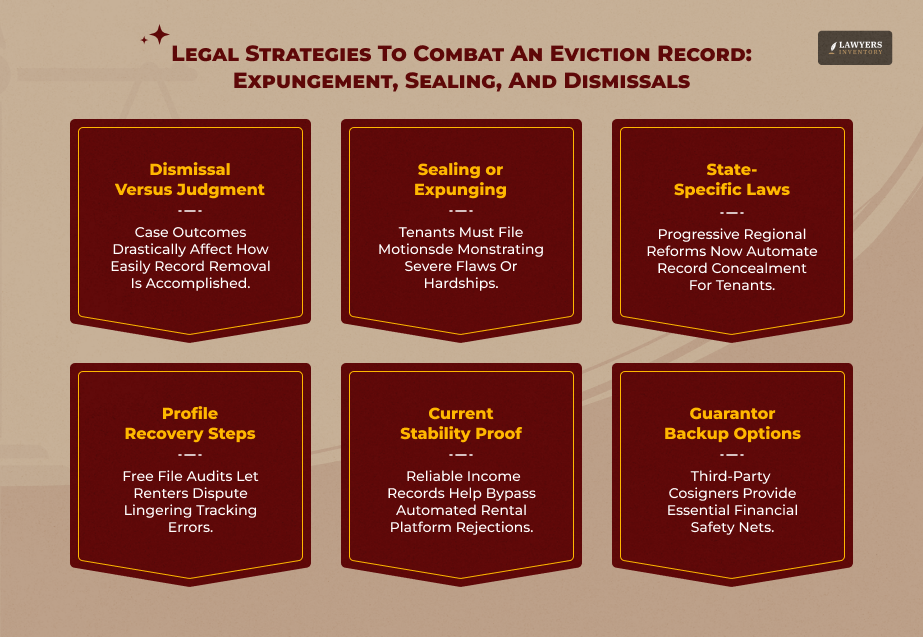

Legal Strategies To Combat An Eviction Record: Expungement, Sealing, And Dismissals

You can avoid an eviction report that dictates your life for seven years.

Based on how the case has ended and the laws of the local jurisdiction, you can follow several legal pathways to hide, neutralize, or clear the record.

1. Dismissal Vs. Judgment

The outcome of an eviction court case will be either a judgment or a dismissal of the case.

Dismissal

Dismissal means that the landlord has dropped the lawsuit, and the tenant has paid the balance before the court date.

Also, dismissal can happen if the tenant wins the case in front of a judge.

Furthermore, when the outcome is dismissal, it means the absence of any formal eviction judgment.

However, the filing of the lawsuit still exists in the public record and can show up on background checks unless action is taken.

Judgment

Judgment means that the judge has given a verdict in favor of the landlord.

When there is a judgment, it means that the tenant has violated the lease or has failed to pay rent.

So, the judge has granted the landlord the legal right to repossess the property. When there is a judgment, the tenant will have a tougher time removing the eviction record in comparison to dismissals.

2. What Is The Process Of Sealing Or Expunging A Record?

Expungement refers to a legal mechanism that removes a court case from the record permanently. However, sealing means removing the record from public view but keeping it accessible for concerned parties, authorized agencies, and court personnel.

When a judge orders the expungement of an eviction record, the court clerk will hide the electronic file, and screening companies will no longer have access to the report.

If you are a tenant and you want to secure an expungement, you will have to file a formal written motion with the civil court that handled the eviction.

However, you will have to meet specific legal criteria to expunge or seal your record legally.

Procedural Flaws

You have to prove that the landlord has failed to provide proper legal notice, for example, a 3-day or 5-day pay-or-quit notice, before filing the lawsuit.

Stipulated Agreements

The tenant and the landlord have to reach an agreement where the tenant will pay the outstanding balance, and in exchange, the landlord will join a mutual motion to seal the case.

Interests Of Justice

A tenant has to convince a judge that the eviction has taken place during an extreme hardship, such as a sudden job loss or medical crisis.

Also, the tenant has to convince that the debt has since been fully paid, and the public availability of the record is causing disproportionate harm to the family’s survival.

Moreover, regarding the role of the court in sealing or expunging an eviction record, the National Center for State Courts says,

“When courts act to seal these records, they affirm that a dismissed or resolved case should not serve as a lifelong barrier to housing.

These benefits must be weighed against the public interest in having access to court records.

Eviction sealing mechanisms can also support effective settlement negotiations and create additional incentives for tenants to comply with the terms of a settlement agreement.

This can be even more effective when used as part of a court-based eviction diversion or mediation program that encourages early resolution of landlord-tenant disputes.”

3. State-Specific Variations In Sealing Laws

Eviction, being a civil legal affair, is highly region-specific.

Furthermore, many states in the USA have recently passed progressive reforms to automate the sealing process and protect tenants from permanent blacklisting.

California

State law automatically seals all eviction filings from the public directory upon submission.

The record only becomes public if the landlord wins the case within 60 days of filing.

If the case is dismissed, settled, or goes unresolved past 60 days, it remains sealed permanently.

Illinois

Under the Illinois Eviction Record Sealing Act, courts are granted broad authority to seal records if the case has been dismissed, if the lease was violated due to domestic violence, or if sealing the record is deemed in the interest of justice.

Minnesota

Minnesota law allows for the mandatory expungement of an eviction if the tenant wins the lawsuit or there is a dismissal of the case.

Expungement also happens if the tenant pays off the debt and waits a specific statutory period.

4. Proactive Recovery: Rebuilding Your Profile

If sealing or expungement of the eviction report does not work, as a tenant, you have to shift your strategy toward manual mitigation and proactive financial rebuilding.

Furthermore, it is challenging but not impossible to secure a safe, reputable apartment even with an active eviction on your record.

Reviewing And Disputing Screening Reports

Often, consumer databases have outdated information. So, if you are a tenant, you must audit your own files routinely.

The federal law allows you to request a free copy of your disclosure file from specialty tenant screening agencies if you have been denied housing based on their data.

Then, you will review your file, and if you find an eviction file older than seven years or a dismissed case marked as judgment, then you will file an official dispute.

Furthermore, the screening bureau then has to investigate and update or delete the unverified information within 30 days.

5. Leveraging Proof Of Current Stability

Suppose you are applying to independent landlords or smaller property management firms.

You can overcome an automated “No” by providing upfront transparency and context.

Moreover, you should assemble a comprehensive physical or digital “renter’s portfolio” to present alongside their application.

Letters Of Recommendation

You can request written character references from your current employer, professional colleagues, or prior landlords who will vouch for your cleanliness, reliability, and character.

Proof Of Stable Income

You can provide tax returns, bank statements, and consecutive months of pay stubs to demonstrate that your current earnings will cover the monthly rent comfortably.

Ideally, showing an income three times the rent amount works.

Detailed Explanations

You can write a formal, objective, and brief cover letter mentioning the exact circumstances behind the past eviction.

You can show a corporate downsizing event, a sudden medical emergency, or a divorce as the reason.

Moreover, you have to mention the proactive steps you have taken since the eviction to ensure your financial stability and security.

6. What Is The Role Of Co-Signers And Institutional Guarantors?

Sometimes, your application can fail to stand on its own merits due to a recent eviction judgment.

Then, a co-signer or a guarantor can bridge the gap.

A co-signer will sign the lease alongside you. Thus, they will legally bind themselves to pay the rent if you default.

Also, a co-signer is usually a trusted family member or a friend with a strong credit report.

However, if you cannot find a co-signer, you can opt for a specialized third-party institutional guarantor service such as the Guarantors or Insurent.

You will have to pay an upfront fee to them, and it is typically a percentage of the annual rent. Then, these corporations will act as your co-signer.

Read Also: Credit One Bank Class Action Lawsuit – Eligibility And Claiming Your Share

The Intersections Of Debt And Bankruptcy In An Eviction Record

A tenant can face long-term financial damage when an eviction involves significant sums of back rent and legal fees.

You have to manage this debt as an important part of resolving the overall eviction footprint.

How Landlords Pursue Eviction Debt

When a court gives an eviction judgment, the landlord can take possession of the property.

However, there is also a money judgment often against the tenant. For this cash collection, a landlord can deploy aggressive legal methods based on the state guidelines.

Wage Garnishment

Wage garnishment means deducting a set percentage of 15 to 25 percent directly from the weekly paycheck of the tenant.

Bank Account Levies

The landlord can secure a court order to freeze the bank account of the tenant and turn over funds sitting in their checking or savings accounts.

Judgment Renewals

A standard credit account can expire after seven years. However, a formal court money judgment can last for 10 to 20 years.

Moreover, in most states, landlords can renew them indefinitely. So, the debt will never expire until you repay it completely.

Using Bankruptcy As A Last Resort

If you are a tenant with an unmanageable debt following an eviction and subsequent lawsuit judgments, you can file for federal bankruptcy for immediate relief.

The court will trigger an automatic stay when a debtor files for Chapter 7 or Chapter 13 bankruptcy.

Now, this stay order can halt all collection efforts, stop wage garnishments, and freeze civil lawsuits.

Moreover, when the bankruptcy process concludes, the tenant’s legal liability for past unpaid rent, utility balances, and landlord legal fees is completely discharged (wiped out).

Also, while the historical record of the eviction lawsuit itself will remain in the public court directory, the associated collection debt is permanently eliminated.

This stops further collection actions and allows the tenant to focus their resources on rebuilding their life.

How Long Does An Eviction Stay On Your Record: Recovering From A Severe Setback

So, for how long does an eviction notice stay on your record?

The Fair Credit Reporting Act dictates 7 years as the span for which an eviction will stay in your record.

However, an eviction record has deeper impacts on the financial, social, and legal aspects of the tenant beyond those seven years.

So, you have to monitor the screening reports actively, seek legal avenues for record sealing or expungement when applicable, and maintain transparency with independent landlords.

In addition, you have to tackle associated debts aggressively to make the recovery process faster and steadier.

Leave A Reply

Hung Jury vs. Mistrial: What Is The Difference And Why It Matters

Read More

NarodniyDimUkraina: An Overview Of The Kyiv-Based Brand Preserving Ukrainian Craftsmanship

Read More

What Is A Mistrial? Legal Definition, Causes, And What Happens Next

Read More

What Is A Sequestered Jury? Legal Definition, Process, And Everything You Need To Know

Read More

What Is A Hung Jury? Legal Definition, Causes, And What Happens Next

Read More

0 Reply

No comments yet.