Today’s topic: When will workers’ comp offer a settlement, and how does the timeline impact employers?

Dealing with workers’ compensation claims is probably one of the most difficult and taxing things for an employer. There is reputation damage, as well as financial damage, that the company needs to go through in such cases.

At such times, having a clear understanding of when workers’ comp will offer a settlement eases the burden on the victim. Additionally, it also impacts the employer who is liable and owes the victim a duty of care.

In this blog, we will talk about the following things:

- The process of a workers’ compensation claim.

- When will workers’ comp offer a settlement?

- How does the timeline impact the employers?

- Strategic defense for employers to manage the burn rate.

- Proactive mitigation strategies for employers.

- When to offer a “nuisance” settlement vs. defending a claim

- The need for MSP compliance in the final settlement.

Therefore, to know about these, keep reading!

Understanding A Workers’ Compensation Claim: From Incident To Resolution

Before we get to answering when will workers’ comp offer a settlement, it is important to understand the stages of the claim.

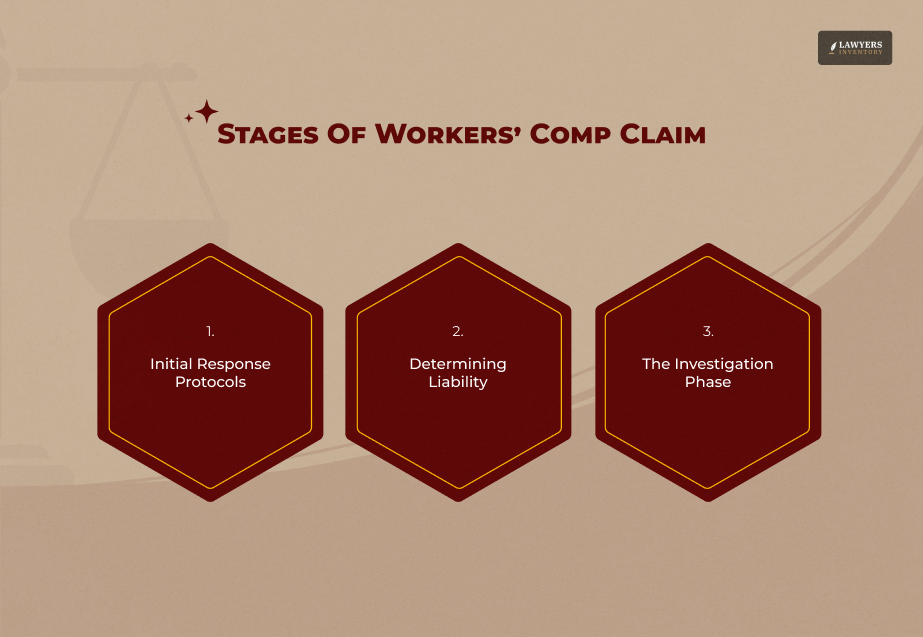

Here are the three stages from the incident to the resolution:

1. Initial Response Protocols

Firstly, reporting the incident within 24 hours of occurrence forms the bedrock of a strong defense for all employers.

This short time frame enables the capture of physical evidence while it is still in its original state. Additionally, it also ensures that witnesses’ statements remain unaffected.

After a certain time, the facts may become unclear. Furthermore, it becomes easier for claimants to exaggerate their symptoms or for “red flags” to remain hidden.

Prompt reporting is a sign of an open culture. And, at the same time, it helps keep the chain of investigation alive.

2. Determining Liability

Secondly, an injury would be eligible for compensation if it fulfills both conditions of the dual prong test. That is, it should arise out of as well as happen in the course of employment. (Source: NCBI)

Essentially, the employment must be the main cause of the injury, not merely the accidental location.

Employers need to carefully ascertain whether the worker was engaged in a company-related activity at the time. Or whether personal, non-work-related elements like pre-existing conditions or playing around were actually responsible for the injury

3. The Investigation Phase

Finally, successful recovery relies on identifying fraud signs promptly. Typical warning signs are as follows:

- “Monday morning” injury reports that supposedly happened late Friday.

- Absence of witnesses.

- Different stories about the event.

Additionally, discrepant medical details or workers with a record of multiple claims should be closely examined.

Immediately recording these irregularities will strengthen the employer’s case in settlement talks or even in court.

When Will Workers’ Comp Offer A Settlement And Why It Affects The Employer?

In workers’ compensation, a settlement refers to a mutual agreement between the parties. Wherein an injured worker agrees to close the claim and forego future benefits in return for a lump sum or structured payments.

When Will Workers’ Comp Offer A Settlement?

There is no fixed timeline under the law for this, but the offers usually happen at certain stages:

- Maximum Medical Improvement (MMI): Settlements are most often proposed after a medical professional has confirmed that the worker’s medical status has been maximally stabilized. And that one should not expect further improvement. At this point, the workers’ need for medical care and level of disability become clear.

- Early in the Claim: Insurers sometimes offer a “quick settlement” option as a way to get out of a case they think might become very costly if it is pursued over a long period.

- During Appeals: If the claim was initially rejected but the insurer thinks the final decision will be in the worker’s favor on appeal, they might offer a settlement as a way of avoiding additional litigation.

- Permanent Disability Classification: Another time a settlement is offered is when a worker is officially classified as permanently partially or totally disabled.

Why Does It Affect The Employer?

The time or schedule of when will workers’ comp offer a settlement heavily impacts the employers. And that is because there would be financial, legal, and operational shifts that the company would have to deal with!

Here are some of the ways in which this impacts the employers:

- Insurance Premium Increases: The history of an employer’s claims is a prime determinant in setting future rates. This is particularly the number and severity of claims that have been settled. A series of settlements or a particularly expensive one usually results in a price hike.

- Experience Modification Factor (Ex-Mod): Claims that have been settled are capable of pushing up an employer’s Ex-Mod. This is a factor that can cause a hike in insurance charges by more than 25% as compared to the industry average.

- Liability Protection: After reaching a settlement, normally, the employee signs away their right to sue the employer for being negligent about that injury.

- Administrative Relief: After agreeing to a settlement, the employer can literally shut the file. Therefore, it puts an end to the employer’s and insurer’s ongoing administrative efforts to manage regular payments and medical supervision.

- Workforce Morale: Although it addresses the monetary commitments, on many occasions, incessantly settling can send safety signals to the other employees or even influence the workplace culture and employee retention.

Strategic Defense Milestones For Employers: Managing The “Burn Rate”

Now that you have a clearer answer to when will workers’ comp offer a settlement, let us talk about what employers can do to manage the burn rate.

Maximum Medical Improvement (MMI) As A Tactical Gatekeeper

Maximum Medical Improvement (MMI) is the ultimate pivot point for any employer looking for a strategic way out.

The moment a doctor declares that a worker’s condition has stabilized, it is a good sign. That’s because the “burn rate” of unplanned medical expenses turns into a fixed liability evaluation of a person.

After getting to MMI, a defense team is able to evaluate the medical needs for the long-term. Additionally, they can change the claim from ongoing treatment to a final settlement.

Utilizing Independent Medical Examinations (IMEs) To Challenge Claims

Secondly, Independent Medical Examinations (IMEs) are a great way to get a second, more neutral opinion when a doctor seems either too cautious or a little unclear in their judgment.

They serve as a foundation for challenging restrictions on work capacity and the ongoing need for treatment.

An IME also has the potential to make a claim less risky by establishing a medically neutral ground for disputing claims of symptoms that are out of proportion or of treatments that are not needed.

Permanent Disability Ratings: Standardizing Settlement Ranges

When MMI is determined, the use of Permanent Disability Ratings that are derived from the workers’ compensation schedules of the state (e.g., California and Texas) can serve as a firm procedural step towards settlement of the dispute. (Source: Withstand Lawyers)

Besides, these ratings represent a means to convert medical results into money through standardized units.

This, in turn, gives the employer the ability to propose settlement accords that are legally permissible and at the same time limit the risk of further expenditure.

Proactive Mitigation Strategies For Employers In Workers’ Comp Claims

There are certain strategies that employers can definitely use to mitigate the risks during a workers’ compensation claim. Here are some of them that you need to know:

Implementing Structured Return-to-Work (RTW) Programs

Return-to-Work (RTW) programs are the strongest weapon employers have in managing the costs related to “lost time”.

Offering accommodations like modified duties or transition roles is, in essence, an instant measure by which businesses slash the Temporary Total Disability (TTD) payments and associated overheads. (Source: MEM)

In fact, the benefits go even beyond mere saving of money. It has been shown that keeping individuals engaged in their work environment results in the prevention of the development of a “disability mindset”.

It also helps in maintaining social connections, and being able to do these three things usually leads to a far shorter final claim closure period.

Breaking The Litigation Cycle With Empathy-Led Communication

Secondly, fear or confusion can be so strong that often it is not greed driving the workers to the lawyer.

Employers who empathize with workers, who are continually there for them, and explain the benefits in clear terms, may save themselves from the conflict that comes with the lawyer.

If the workers trust, the chances of them deciding to sue go down. Additionally, the process of the settlement can go on without the worker putting up a fight.

Leveraging Technology And AI In Claims Management

Finally, contemporary defense strategies make use of AI analytics to uncover ‘creeping catastrophes’.

Such tools tirelessly go through the contents of medical records and adjuster notes so that they can detect and flag high-risk claims even before the damage costs the most.

For instance, claims with multiple medical conditions or claims with difficult patients are examples of high-risk claims.

Through early detection and automated document review, employers can use technology as a tool to come in at the right time with the right resources and turn around the claim so that it doesn’t get out of hand.

When To Offer A “Nuisance” Settlement Vs. Defending The Claim

The decision to settle often depends on the “burn rate” – the continuous cost of legal fees and administrative oversight versus the price of a quick exit.

In that regard, a “nuisance” settlement is a tactical instrument for low-value or legally questionable claims.

By presenting a small cash payment early on, an employer can shut down a case that would otherwise exhaust the company’s resources through a lengthy litigation, even if the defense is likely to win.

On the other hand, if a claim results in a major permanent disability or a dangerous precedent is set for the workforce, a strong and well-documented defense should be the priority.

If every minor claim is settled, it may, without intention, send out the message of a “pay-day” culture, leading to more filings.

Hence, the employers should consider the short-term financial gain of a settlement against the long-term effects on their Experience Modification Factor (Ex-Mod) and future premiums.

A smartly executed defense does not only safeguards the financials but also the integrity of the workers’ compensation programs.

Need For Medicare Secondary Payer (MSP) Compliance In Final Settlements

Going through final settlement processes involves compliance with the Medicare Secondary Payer (MSP) law without any compromise.

If a settlement takes care of the children’s medical care benefits in the future, the involved parties must take a point Medicares interests.

In this case, Medicare acts as a secondary payment source, implying that it should not carry the burden of medical expenses that are meant to be paid off by a workers’ compensation settlement.

Besides risking a situation where Medicare refuses to pay for injury-related healthcare of the worker, non-compliance also exposes the employer to a lawsuit where they can even be liable to pay double damages.

To reduce this exposure, employers turn to a Workers’ Compensation Medicare Set-Aside (WCMSA). Here, an account is set specifically for medical expenses related to an injury for the rest of the employee’s life that Medicare would have covered.

Accurate records and approval from CMS give you the “safe harbor” in the settlement. Therefore, you may not have to worry about the federal government coming in later.

Leave A Reply

Home Insurance For First-Time Buyers: A Beginner’s Guide

Read More

The Most Common Workplace Injuries That Qualify For Workers’ Compensation

Read More

When To Hire A Workers’ Compensation Lawyer After A Job Injury

Read More

0 Reply

No comments yet.