Today, we talk about deferred compensation.

As demonstrated by the cases of 2026 Morgan Stanley lawsuit, your deferred compensation will never be completely safe until it finds its way into your bank account.

Financial planning involves long-term considerations when it comes to managing deferred compensation schemes. In the USA, these plans are not simple postponements of payrolls.

Rather, they are sophisticated agreements that fall under strict US federal tax rules and regulations.

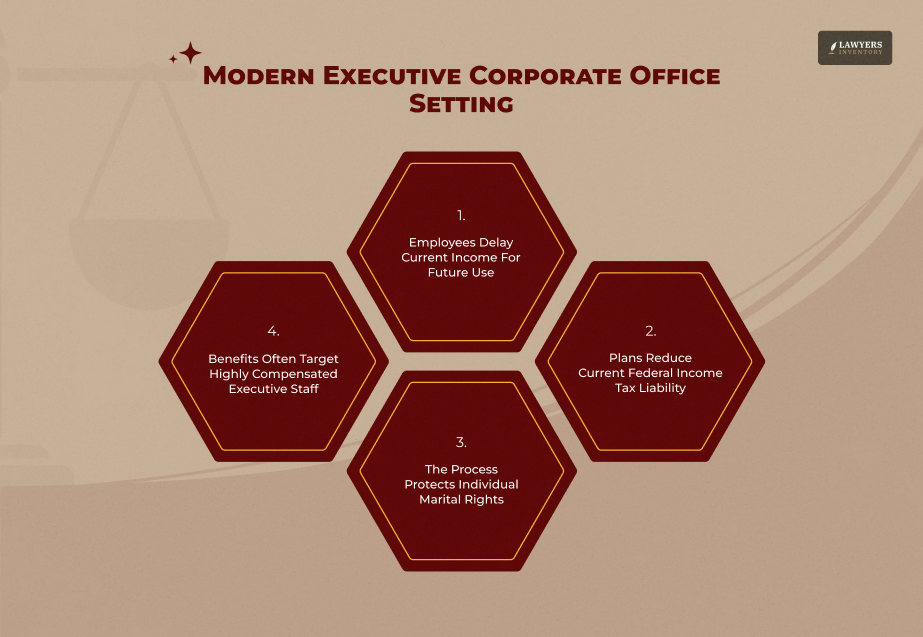

Under a deferred compensation scheme, you can earn income in one year while receiving it at a later stage, which helps provide a huge tax break.

This scheme has been known to offer a number of benefits to employees since the money belongs to the employer before it reaches the beneficiary on the payment date. At present, there are several cases of major lawsuits related to determining whether some of these programs can be classified as ERISA programs or simply bonuses.

In this article, we will elaborate on the following:

- The critical differences between qualified and nonqualified plans.

- Federal statutes like IRC Section 409A and ERISA govern these payouts.

- Common legal pitfalls and the “trouble zones” of corporate insolvency.

- Recent judicial landmarks and active litigation affecting payment security.

What Is Deferred Compensation?

Deferred compensation can be said to be a financial technique adopted by companies for attracting and retaining the best talent. Essentially, deferred compensation is a form of “deferred payment” which occurs in due time, say during retirement or on a certain milestone.

The Fundamental Principle Of Deferred Compensation

Essentially, being involved in a deferred compensation plan means you choose to defer part of your pay or bonus at present.

To get a good understanding of deferred compensation, it helps first of all to know that you are lending your own company money.

Tax Savings For Wealthy Individuals

The main attraction of deferred compensation lies in its capacity to reduce your current tax liabilities. The hope here is to be able to pay yourself at the lowest rate possible in future years as you approach your retirement period. (Source – ADP)

Understanding The Types Of Plans

Before entering into any deal, it is imperative to understand what constitutes a deferred compensation plan within your particular employment agreement. Typically, there are two primary forms of such plans: Qualified and Nonqualified.

Qualified Deferred Compensation Plan

The qualified deferred compensation plan includes 401(k), 403(b) accounts, and others, which adhere to rigid nondiscrimination criteria and are accessible to all employees.

The money saved under such plans is placed in a trust, which ensures that it is safe even in cases where the corporation faces bankruptcy.

Nonqualified Deferred Compensation Plans (NQDC)

The NQDC plan is commonly known as a “top-hat” plan and targets senior executives only. Such plans have no contribution caps but do not enjoy the same legal safeguards, and the money remains the company’s general property.

Laws On Deferred Payments

In terms of the deferred compensation legislation, both IRC and ERISA are extremely important as they determine when employees will get access to funds and the level of taxes they must pay.

IRC 409A – Golden Rule

This section is perhaps the most important regulation regarding deferred compensation as far as federal law is concerned.

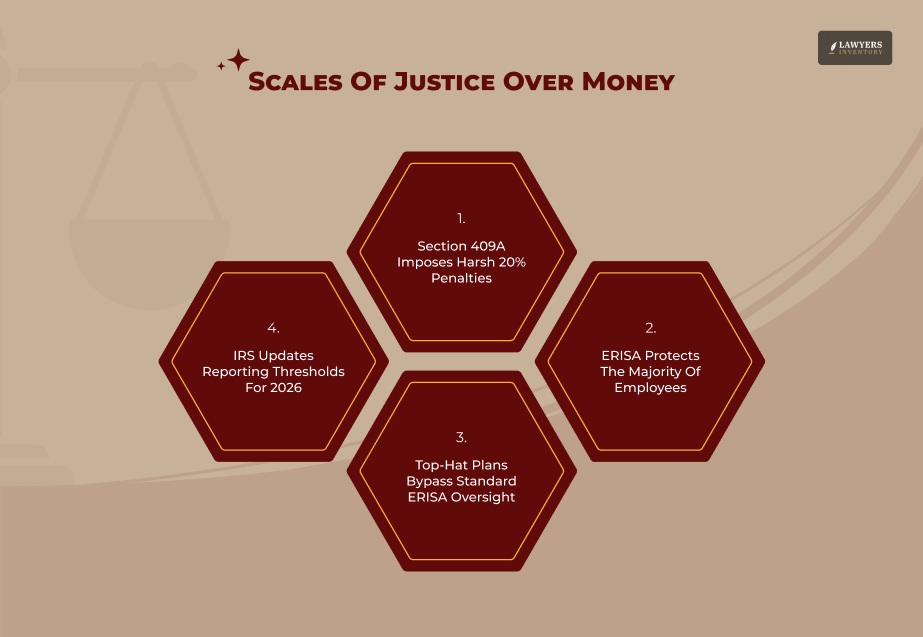

Under IRC 409A, strict rules are placed with regard to timing. Employees who fail to comply with 409A are required to immediately pay taxes on deferred amounts and also face a 20% penalty. In 2026, the IRS tightened its regulations on NQDC to maintain compliance (IRS).

ERISA Protections And Exceptions

Under ERISA, fiduciary and vesting standards are applied to all qualified plans. However, in most cases, NQDC plans are created in such a way that they are exempt from ERISA in order to provide some flexibility.

That is precisely why Sheresky v. Department of Labor litigation takes place from 2025-2026 since advisers argue that they should be entitled to pension protections (PLANSPONSOR).

Why A Substantial Risk Of Forfeiture Matters

A Substantial Risk of Forfeiture is a legal condition where your right to the money depends on future performance or remaining with the company.

If this risk disappears (for example, if you become fully vested), the IRS may view the money as current income unless your deferred compensation plan is drafted under Section 409A.

2026 Legal Update – The Fight For Payout Security

As of April 2026, the legal landscape is shifting rapidly. The Cunningham v. Cornell University (2025) Supreme Court ruling has made it significantly easier for employees to sue over “prohibited transactions” within their retirement structures.

This ruling is now being used as a blueprint for a new wave of lawsuits against firms that use “forfeiture accounts” to reduce their own corporate contributions rather than benefiting the employees (Willkie Farr & Gallagher).

The Morgan Stanley Case And The “Bonus” Loophole

The ongoing 2026 arbitration involving former Morgan Stanley advisers is a warning to all executives. The firm argued that certain payouts were “bonuses” and not “pensions,” allowing them to cancel the pay when advisers left for competitors.

This case is critical because it will decide if non-qualified deferred compensation can be protected by ERISA’s anti-forfeiture rules.

New IRS Wage Reporting For July 2026

Beginning in July 2026, the IRS is rolling out updated reporting requirements for deferred compensation via the SECURE 2.0 Act.

These changes, reflected in the revised 2026 General Instructions for Forms W-2 and W-3, require more granular tracking of “catch-up” contributions for high earners (IRS).

What Is The Best Way To Secure My Deferred Payout?

In our experience assisting high-net-worth professionals, the first 48 hours of a company’s insolvency filing are the most critical for your assets.

You should ensure your agreement includes a Rabbi Trust with an in-service”distribution trigger for emergencies.

While no plan is 100% safe from a company’s creditors, a well-structured vesting schedule can help you pull funds out gradually before a financial crisis hits.

Frequently Asked Questions (FAQs):

Understanding the complexities of deferred compensation is vital for long-term security. Here are a few final points that citizens often find confusing.

For qualified plans like 401(k)s, the limit is $24,500. Nonqualified plans generally have no federal contribution limit (IRS).

No, a Rabbi Trust only protects you from the employer changing their mind, not from the employer’s creditors in bankruptcy.

Unlike a 401(k), nonqualified plans are not eligible for IRA rollovers. They are paid out as taxable W-2 income.

Generally, no. Under Section 409A, you must stick to the pre-set distribution schedule unless you have a qualified unforeseeable emergency.

This depends on your contract. Some plans have “clawback” or forfeiture provisions if you are terminated for cause.

Usually, if you receive the payout over ten or more years, it is taxed in your current state of residence.

No. Section 409A strictly prohibits the acceleration or further deferral of payments once the schedule is locked in.

Leave A Reply

Hung Jury vs. Mistrial: What Is The Difference And Why It Matters

Read More

NarodniyDimUkraina: An Overview Of The Kyiv-Based Brand Preserving Ukrainian Craftsmanship

Read More

What Is A Mistrial? Legal Definition, Causes, And What Happens Next

Read More

What Is A Sequestered Jury? Legal Definition, Process, And Everything You Need To Know

Read More

What Is A Hung Jury? Legal Definition, Causes, And What Happens Next

Read More

0 Reply

No comments yet.