Today’s topic: Is Super.com legit?

I have tracked consumer trends for years. Furthermore, I analyze expert legal opinions daily. Recently, I noticed a troubling change in online shopping. Buying items online used to be simple. Today, however, platforms use complex tech systems and hidden rules.

Super.com is a prime example of this shift.

It started as Snaptravel under Snapcommerce, Inc. Consequently, the app has expanded into financial tools. As a result of this expansion, frustrated travelers often ask a simple question: Is Super.com legit, or is it a scam?

To find out, I studied the platform’s data. Additionally, I reviewed current marketplace regulations. The reality, therefore, is not a simple binary choice. Super.com is a legally registered business entity. In fact, major venture capital firms fund it.

However, its massive digital contract reveals a clear strategy. Specifically, Super.com shifts all transaction risks onto the consumer. The platform offers low prices but, in turn, removes your legal rights.

Therefore, to understand your rights in 2026, look past the marketing. We must inspect the fine print carefully instead.

Quick Verdict: Is Super.com Legit And Safe To Use?

Personally, from what I have examined, I find that Super.com is safe and legally registered. Specifically, major institutional venture capital firms fully fund the platform. Therefore, it is definitely not an unregistered scam.

However, the company operates under an aggressive corporate risk-shifting model instead. Consequently, they pass all travel and financial liabilities directly onto you.

In short, the business is completely legitimate. Yet, your traditional consumer protection rights are entirely removed in exchange for cheap discount rates.

Thus, you save money but lose your legal safety nets. As a result, I recommend reviewing their baseline metrics below first.

Baseline Legitimacy Metrics

• Corporate Registration: Valid status under Snapcommerce, Inc. and Snapmoney, Inc.

• Venture Financial Backing: High equity. Backed by major institutional investment firms.

• Travel Operational Model: High risk. Operates strictly as a third-party intermediary broker.

• Fintech Service Status: Legitimate partnership. Accounts managed via Republic Bank & Trust Company.

• Consumer Legal Recourse: Low protection. Mandates individual private arbitration instead of courts.

Understanding Contract Privity: Why Travelers Get Stranded

Thousands of users leave bad reviews on Trustpilot. Similarly, they complain to the Better Business Bureau.

For instance, a traveler books a hotel room or flight. They receive a confirmation email. Then, they arrive at the hotel counter. Unfortunately, the clerk finds no record of the booking.

To consumers, this immediately feels like an intentional scam. On the other hand, contract law explains the real cause. The issue, specifically, is a total lack of contract privity.

Super.com explicitly states its role in the travel terms. For example, it operates strictly as a broker. The company terms say:

“Super.com does not provide you with hotel accommodations, flights, or other Travel Services offered through Super.com; hotel accommodations, flights, and related services are provided by the relevant supplier.”

(Source: Terms & Conditions, Legal)

Consequently, when you click book, you enter a multi-party contract. You do not contract with Super.com for lodging. Instead, your contract is directly with the hotel or airline. Often, it is with wholesale distributors like Expedia Group, Inc.

Hotels frequently overbook their available rooms. Therefore, they must choose which reservations to honor. Naturally, they prioritize guests who booked directly at full price. As a result, they bump guests who used third-party discount brokers.

Ultimately, Super.com’s contract completely shields the company from these failures. The terms state they bear no liability for supplier errors. Furthermore, they will not pay for emergency relocation costs if a hotel turns you away. Consequently, you must solve the issue alone.

The Fine Print Reality Of Common Complaints

Digital marketplace laws allow companies to enforce strict terms. Therefore, a wide gap exists between consumer expectations and legal reality. Let us break down three major complaints using the text.

1. Sudden Cancellations After Confirmation

Many users feel outraged when Super.com cancels a confirmed reservation. To a buyer, a confirmation email means a final deal.

However, Super.com protects its software with an “Obvious Error” clause. The platform keeps the unilateral right to cancel any booking. For example, they can void the deal after confirmation if their system glitches.

In standard contract theory, confirmation means an offer and acceptance. In contrast, Super.com’s terms change this rule. The clause acts as a condition subsequent. Consequently, the platform legally cancels the transaction without penalty.

2. Denied Refunds And The Forfeiture Trap

The platform heavily markets its Limited Bookings Guarantee. On the surface, it looks like a safety net for travelers. Yet, the strict rules turn it into an obstacle course.

The terms require you to call Super.com immediately from the hotel desk. If you walk away and book another room, you forfeit your rights. As a result, you lose the guarantee completely.

In addition, minor mistakes also void the guarantee. For instance, your name must match your physical ID perfectly. Furthermore, you must be over 18 years old. Finally, you must provide a credit card for local resort fees.

3. The Super+ Membership Subscription Roll

Consumers frequently report unexpected monthly charges of $15. Moreover, they do not remember signing up for a premium plan.

This issue involves Federal Trade Commission guidelines on dark patterns. Specifically, Super.com uses automated consent boxes during travel checkouts. These boxes bundle the Super+ Membership automatically.

Consequently, completing a travel purchase activates a trial period. The trial automatically rolls into a paid monthly subscription unless you opt out. The path is legal but lacks transparency.

The Fintech Pivot: Snapmoney, Inc. And the Data-for-Credit Trap

Super.com is no longer just a travel search engine. Instead, the company has shifted toward financial technology and data monetization.

The financial pages introduce a new corporate entity. Consequently, you sign a binding contract with Snapmoney, Inc.

This pivot changes the regulatory landscape. As a result of which, the platform must follow federal lending laws and credit reporting acts.

Super.com is not a bank. Rather, they partner with Republic Bank & Trust Company to offer financial products. This partner issues the Super.com Deposit Account and Secured Charge Card.

The partnership acts as a shield. Specifically, Republic Bank holds the funds and manages credit risks. Meanwhile, Super.com operates the user interface. This layout keeps the bank safe from daily consumer complaints.

The real consumer risk hides inside the Earnings Services. Super.com offers cash rewards for playing mobile games or taking surveys.

However, the legal mechanics show Super.com acts as a data router. Clicking an earnings task opens an external ad network. Then, a disclaimer warns that you are leaving Super.com.

Super.com disclaims all liability for third-party data tracking. Consequently, you trade your personal data for app credits.

Section 5 details a harsh account termination clause. Specifically, Super.com can freeze your user account at any time. If they close your account, you lose all wallet credits instantly. Therefore, the platform bears no liability for your financial losses.

Furthermore, cashing out your credits can take up to 45 days. This long delay favors corporate liquidity over your wallet.

State-Level Consumer Disclosures: Where You Live Matters

E-commerce contracts include regional variations. Because Super.com manages credit tools, Section 10 outlines mandatory State Disclosures. Therefore, your legal protections depend on your home state:

- New York and Vermont: The platform pulls credit reports only for valid reviews. In addition, the contract directs New York users to the New York State Department of Financial Services for rate tools.

- California and Utah: The fine print serves as a warning. Specifically, Super.com sends negative credit reports to national agencies if you default on obligations.

- New Jersey: State laws limit corporate waivers. Therefore, the contract notes that liability caps only apply as far as New Jersey law allows.

- Washington State: The platform complies with statute RCW 63.14.167. Consequently, residents do not pay interest fees caused by merchant refund delays. (Source: Washington State Legislature)

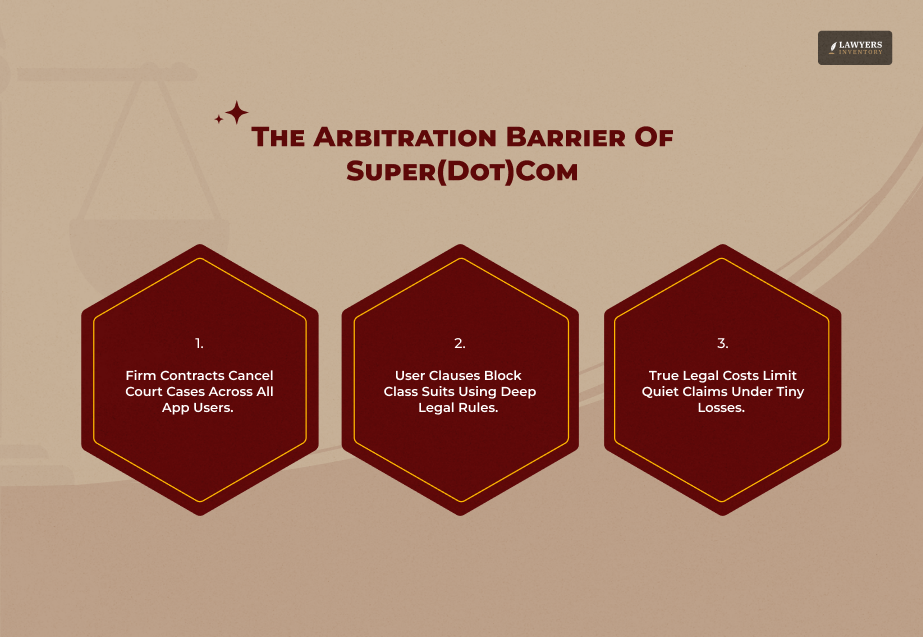

Total Recourse Lockout: The Arbitration Barrier

Super.com prints its most severe restrictions in all-capital letters. Specifically, the platform applies a strict Mandatory Arbitration Provision and Class Action Waiver across all services.

By using the app, you agree to these limits:

- No Jury Trials: You waive your right to file a lawsuit in court.

- No Class Actions: You waive your right to join other users in a group lawsuit.

- Private Arbitration: Instead, you must resolve all disputes alone through private tribunals.

Most travel disputes involve small amounts between $100 and $1,000. Therefore, hiring a private arbitrator costs more than the value of the lost booking. As a result, this rule stops most consumers from taking action.

The Military Lending Act (MLA) Exception

The Terms & Conditions page of the platform contains a critical federal exception. The mandatory arbitration clause does not apply to active-duty service members or dependents.

Consequently, covered borrowers keep their right to sue in court. Furthermore, the law caps their maximum credit costs at 36% APR.

Real Cases Of Super.Com Complaints

When I searched online for “Is super.com legit?,” one of the first few pages that I clicked was our most trusted forum – Reddit. And it did not disappoint me.

For instance, a California traveler recently detailed a harrowing ordeal. The user booked two Manhattan hotel rooms through Super.com for a family trip. They paid in full and even confirmed the rooms directly with the hotel beforehand. (Source: Reddit)

Unfortunately, the nightmare began at check-in.

The hotel front desk revealed that Super.com had secretly canceled one of the rooms days earlier. Furthermore, according to the user, the platform pocketed the money without issuing them a refund or notification.

Consequently, the user spent over three hours stranded in the lobby with exhausted children. Ultimately, the family had to book a last-minute room at a nearby hotel for $403.96 out of pocket.

When the victim asked for legal options, a seasoned community user highlighted the brutal reality of Super.com’s Terms of Use (TOU):

- Delaware Arbitration Lock: The TOU forces mandatory arbitration in Delaware, making traditional litigation economically impossible for a few hundred dollars.

- Section 1542 Waiver: Shockingly, users waive rights under California Civil Code Section 1542, shielding the company from liability for automated booking glitches.

Given these contractual limitations, consumers often explore alternative resolutions.

This may include filing formal complaints with consumer protection agencies or contacting financial institutions to discuss transaction dispute processes available under banking regulations.

Read Also: Shein Lawsuit: Copyright, Consumer Claims, And All Major Legal Battles

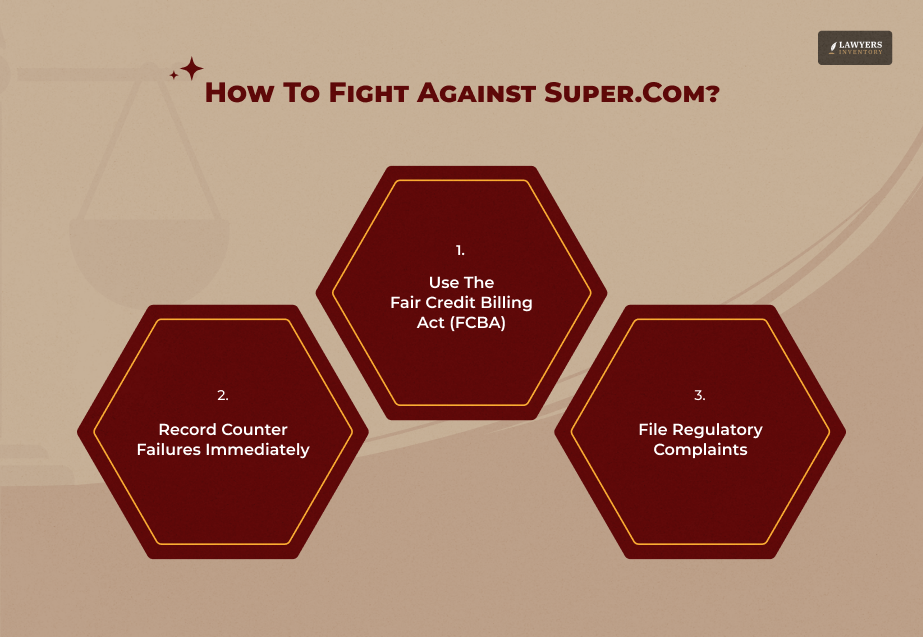

Actionable Legal Remedies: How To Fight Back

Super.com is a highly insulated corporate broker.

So, is Super.com legit? Yes. It is not an illegal operation. However, you can use three strong legal remedies if a transaction fails:

1. Use The Fair Credit Billing Act (FCBA)

If Super.com charges you but the hotel loses the booking, skip their chatbots. Instead, file a formal billing dispute directly with your credit card bank.

The FCBA gives you the right to dispute charges for undelivered services. Consequently, the bank will freeze the funds during an investigation.

2. Record Counter Failures Immediately

To protect your guarantee rights, follow their precise rules. For instance, stay at the hotel counter.

Next, document the time. Then, call customer support at 1 (877) 376-2710. Note the names of the hotel staff. Gather proof before you leave the building.

3. File Regulatory Complaints

If you face hidden fees or deceptive subscription paths, report the issue. Specifically, file a complaint with the Federal Trade Commission and your state Attorney General. High complaint volumes trigger formal state investigations.

Super.com offers cheap rates by removing your legal safety nets. Therefore, if you use the platform, protect yourself. For example, use a premium credit card. Buy independent travel insurance. Always call the hotel directly to confirm your room before you travel.

Disclaimer: The information provided in this article is for general informational purposes only. It does not, and is not intended to, constitute legal advice. Please consult an attorney for legal help.

Leave A Reply

Hung Jury vs. Mistrial: What Is The Difference And Why It Matters

Read More

NarodniyDimUkraina: An Overview Of The Kyiv-Based Brand Preserving Ukrainian Craftsmanship

Read More

What Is A Mistrial? Legal Definition, Causes, And What Happens Next

Read More

What Is A Sequestered Jury? Legal Definition, Process, And Everything You Need To Know

Read More

What Is A Hung Jury? Legal Definition, Causes, And What Happens Next

Read More

0 Reply

No comments yet.