Non qualified deferred compensation plans are excellent financial tools. They help highly paid executives who have hit the ceiling on the number of contributions allowed for their 401(k) savings plans for the year.

As of 2026, the use of a non qualified deferred compensation plan has become quite important. It is so especially after the recent rise in the 401(k) elective contribution ceiling to $24,500 by the IRS.

Although it is indeed a relatively small amount of money considering a CEO’s earnings. (Source – Raymond James)

This arrangement allows individuals to defer receipt of a share of their wages or bonuses to some future date, thereby reducing their taxable income at the time.

Nevertheless, in contrast to regular pension plans, a non-qualified deferred compensation plan entails the risk of business failure. Here, the money continues to be part of the corporation’s assets.

Legal issues related to the legality of such programs can be seen in contemporary court cases like Sheresky vs. Department of Labor, which was brought to court in December 2025 and is currently in motion in March 2026. (Source – Benefits Link)

In this article, we will elaborate on the following:

- The legal distinctions between qualified and nonqualified retirement structures.

- Federal regulations, including IRC Section 409A and ERISA exemptions.

- The impact of recent Supreme Court rulings on plan litigation.

- Strategies for securing payouts through specific trust arrangements.

The Legal Structure Of A Non Qualified Deferred Compensation Plan

Non qualified deferred compensation plans represent a form of agreement between an employer and his/her employee whereby the payment of compensation will be deferred.

Since these plans do not fulfill all the qualifications for Internal Revenue Code Section 401(a), therefore, they do not have any tax advantages like the 401(k).

Unfunded Promise

It should be noted that a non-qualified deferred compensation plan always involves unfunded promises. That means the employee has nothing more than a mere promise to pay from his/her employer.

There are no funds reserved in the account of such an individual under such a scheme. In case of any bankruptcy, the individual under a non qualified deferred compensation scheme will remain an unsecured creditor. (Source – Fidelity Investments)

Distinguishing Nonqualified Deferred Compensation

It is crucial to note that non qualified deferred compensation arrangements are frequently designed for a limited and selective group of individuals called the top-hat class, consisting of management or high-ranking workers.

Through excluding other employees from participating in the plan, a non qualified deferred compensation plan can circumvent most of the cumbersome compliance costs under the federal labor law regulations.

The Constructive Receipt Doctrine In Executive Deferrals

The effectiveness of the non qualified deferred compensation plan lies in its complete avoidance of the Constructive Receipt Doctrine.

It is an IRS regulation requiring that any income be taxed as soon as it is set apart or put aside for your access and availability without significant restrictions.

Under the IRS ruling, once the agency determines that you had the exclusive right to withdraw your wages by 2026, you will be immediately taxed even before you accessed the money.

To defer taxes on your income, your contract should prohibit you from receiving your wages before a certain future date or event. (Source – IRS)

Understanding The Substantial Risk Of Forfeiture

If an individual’s non-qualified deferred compensation plan is going to stay free from tax consequences, then the right to payment needs to be Subject To Substantial Risk Of Forfeiture.

What this means in simple terms is that you do not get your right to the benefit unless you render substantial future services, like sticking around for five years in the organization.

The moment the risk lapses when you have rendered sufficient service, the non-qualified deferred compensation plan stays deferred even if it is subject to tax under 409A.

However, prior to the lapse of the risk, this is what keeps the IRS from treating the benefit as income.

Non Qualified Deferred Compensation Plan: What Are The Laws Protecting You?

The legal landscape for a non-qualified deferred compensation plan is primarily governed by the Internal Revenue Code (IRC) and the Employee Retirement Income Security Act (ERISA).

Understanding these statutes is vital for any participant who wants to avoid a surprise 20% tax penalty.

The Role Of IRC Section 409A

IRC Section 409A is the most critical federal statute regarding any non-qualified deferred compensation plan.

It dictates the timing of deferral elections and the permissible events for distribution, such as separation from service or a fixed date.

If a non qualified deferred compensation plan fails to comply with these strict timing rules, the employee must pay immediate income tax on all deferred amounts plus a 20% penalty and interest.

ERISA Top-Hat Exemptions

Most executives want their non-qualified deferred compensation plan to be exempt from the substantive portions of ERISA.

To qualify as a top-hat plan, the non qualified deferred compensation plan must be unfunded and maintained primarily for providing deferred compensation for a select group of management.

This exemption allows the non-qualified deferred compensation plan to skip the strict vesting and funding rules that apply to 401(k) plans.

The SECURE 2.0 Pivot – Mandatory Roth Catch-Ups In 2026

As of January 1, 2026, the non-qualified deferred compensation plan has become a vital fallback for high-earning executives.

Under Section 603 of the SECURE 2.0 Act, a massive shift has hit the 401(k) landscape. Any participant whose FICA wages exceeded $145,000, indexed to $150,000, for 2026 in the previous year must now make their catch-up contributions on a Roth (after-tax) basis. (Source – Fidelity Investments)

The Tax Shield Gap For High Earners

For decades, executives relied on pre-tax catch-up contributions to lower their taxable income in their highest-earning years.

Now that the IRS mandates these contributions be made with after-tax dollars, the non-qualified deferred compensation plan remains the only vehicle offering unlimited, pre-tax deferral without a Roth mandate.

This makes the NQDC a tax shield of last resort for those looking to keep their 2026 tax bracket as low as possible.

409A Material Event Triggers And Valuation Refreshers

Maintaining a non qualified deferred compensation plan requires constant vigilance over corporate valuations. While many believe a 409A valuation is set it and forget it for a full year, the reality in 2026’s volatile market is far more dangerous.

A 409A valuation only provides Safe Harbor protection for 12 months, or until a Material Event occurs or whichever comes first (Morgan Stanley).

Avoiding The 20% Stale Valuation Penalty

A Material Event is basically a business change. It can include “an acquisition offer, a Series C funding round, or even some kind of secondary stock sale”. (Source-Carta)

If your firm closes a funding round in May 2026, your January valuation is legally stale.

Granting options or setting strikes under an outdated non qualified deferred compensation plan valuation will immediately trigger the Section 409A penalty: 20% additional tax plus back interest for the employee.

Landmark Cases And 2026 Up To Date Litigation

The security of a non-qualified deferred compensation plan often hinges on judicial interpretation of whether the plan is a bonus or a pension.

Recent years have seen a surge in litigation as employees fight to protect their deferred earnings from being forfeited.

The Sheresky v. Department Of Labor Dispute (2026)

One of the most significant cases currently unfolding is Sheresky v. Department of Labor. This lawsuit, which saw a major motion to dismiss filed by the government in March 2026, challenges an advisory opinion regarding Morgan Stanley’s deferred pay structures.

The plaintiffs argue that their non qualified deferred compensation plan should be treated as an ERISA-protected pension plan, which would prevent the firm from clawing back or canceling the pay if the employee leaves for a competitor.

Impact Of Cunningham v. Cornell University

While Cunningham v. Cornell University (2025) primarily dealt with 403(b) plans, its prohibited transaction logic is bleeding into the world of the non qualified deferred compensation plan.

The Supreme Court’s decision made it easier for plaintiffs to sue over plan fees and management, putting plan sponsors on high alert. (Source-J.P. Morgan Asset Management)

If a non qualified deferred compensation plan is found to have even minor ERISA ties, it could open the door for similar high-stakes class actions.

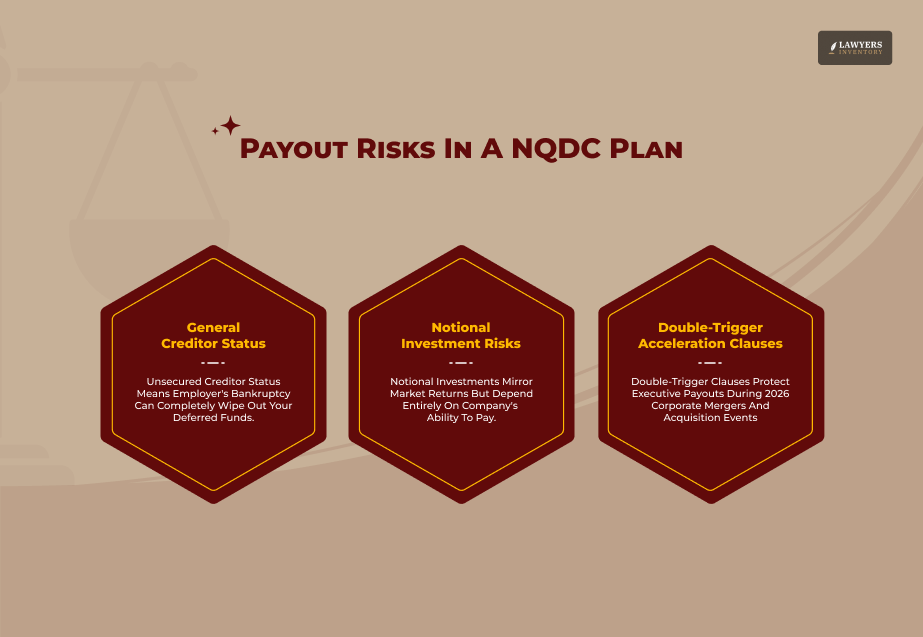

Practical Payout Risks In A Non Qualified Deferred Compensation Plan

Despite the tax benefits, a non qualified deferred compensation plan is only as strong as the company that offers it. Because the money is not in a protected trust, participants must monitor the financial health of their employer closely.

The Danger Of The General Creditor Status

If your employer files for Chapter 11 bankruptcy, the funds in your non-qualified deferred compensation plan can vanish.

Unlike a 401(k), where the money is yours regardless of the company’s fate, the non-qualified deferred compensation plan is just an entry on a ledger.

You have no legal claim to specific assets unless a Rabbi Trust is in place, and even then, creditors can seize that trust in a total liquidation.

Understanding Notional Investments

In a non qualified deferred compensation plan, you usually invest your deferrals in notional funds that mirror the stock market.

However, you aren’t actually buying the stocks. The company is just tracking what the value would be.

If the company’s own investments fail, they may still owe you the money, but their ability to pay the non-qualified deferred compensation plan balance becomes highly questionable.

The Double-Trigger Acceleration Clause Strategy

In 2026, savvy executives are negotiating Double-Trigger acceleration clauses into their nonqualified deferred compensation plan.

This clause ensures that your unvested deferred pay becomes 100% vested and payable only if two specific events occur. This protection is critical during the current wave of 2026 corporate mergers and acquisitions.

Balancing Security And Talent Retention

The first trigger is usually a Change in Control (the company is sold). The second trigger is the Involuntary Termination of the executive without cause.

This structure is superior to a single-trigger because it protects the executive from being purged by new management. It assures the acquiring company that key talent won’t simply walk away with a massive payout immediately after the deal closes.

Strategies To Secure Your Deferred Payouts

To mitigate the risks of a non qualified deferred compensation plan, savvy executives look for specific contractual safeguards. These protections can help bridge the gap between a promise and a guaranteed check.

Utilizing A Rabbi Trust

A Rabbi Trust is a popular way to support a non-qualified deferred compensation plan. In this setup, the employer puts assets into a trust to pay for the non qualified deferred compensation plan liabilities.

While this protects the money from the employer changing their mind, the assets are still subject to the claims of the employer’s creditors in bankruptcy.

Change Of Control Triggers

Many participants in a non qualified deferred compensation plan negotiate for a Change of Control provision.

This ensures that if the company is sold, the non-qualified deferred compensation plan balance is paid out immediately or fully funded.

It prevents a new owner from canceling the compensation plan or altering the payout schedule.

State-Specific Tax Traps And The 10-Year Rule

One of the most overlooked benefits of a nonqualified deferred compensation plan is the ability to escape high state taxes in places like New York or California.

Under federal law (4 U.S. Code § 114), a state cannot tax the retirement income of a non-resident if that income is paid out in a specific way.

Using The 10-Year Installment Strategy

To trigger this federal protection, you must elect to receive your nonqualified deferred compensation plan payout in substantially equal installments over a period of 10 years or more.

For example, if you earn your pay in California but move to tax-free Florida for retirement, California cannot tax those payments as long as they meet the 10-year requirement.

Choosing a lump sum, however, allows your source state to take a massive bite out of your wealth.

Read Also: What Is OASDI? A Complete Guide To Your Social Security Benefits

Frequently Asked Questions (FAQs):

Understanding the complexities of a non qualified deferred compensation plan is essential for any high-earning citizen managing their long-term wealth.

These questions address the most popular issues people face with a non qualified deferred compensation plan.

No, you cannot roll over these funds into an IRA because a non qualified deferred compensation plan is not a qualified plan.

Your non qualified deferred compensation plan agreement dictates this; some allow payouts upon termination, while others might force a forfeiture.

Yes, Social Security and Medicare taxes are typically withheld in the year you defer the income, not when paid.

By deferring income into a non qualified deferred compensation plan, you reduce your current adjusted gross income, potentially keeping you in a lower tax bracket for the current year.

The primary risk is a 20% federal penalty plus interest if the non qualified deferred compensation plan violates strict IRS rules regarding the timing of payments.

Generally, no.

Most non-qualified deferred compensation plan structures are top-hat plans, which are exempt from the majority of Department of Labor fiduciary and funding protections.

An employer typically cannot cancel a non-qualified deferred compensation plan without paying out the vested balance, unless the contract contains specific bad actor or non-compete forfeiture clauses.

Leave A Reply

Hung Jury vs. Mistrial: What Is The Difference And Why It Matters

Read More

NarodniyDimUkraina: An Overview Of The Kyiv-Based Brand Preserving Ukrainian Craftsmanship

Read More

What Is A Mistrial? Legal Definition, Causes, And What Happens Next

Read More

What Is A Sequestered Jury? Legal Definition, Process, And Everything You Need To Know

Read More

What Is A Hung Jury? Legal Definition, Causes, And What Happens Next

Read More

0 Reply

No comments yet.