Is long term disability taxable in the United States?

This is a question that has been making the rounds for a while. And there are several reasons for that to happen.

For you to understand what I am talking about, let me give you a small example. For once, let us try to imagine waking up one day and realizing you can’t go to work anymore because of a serious injury or illness.

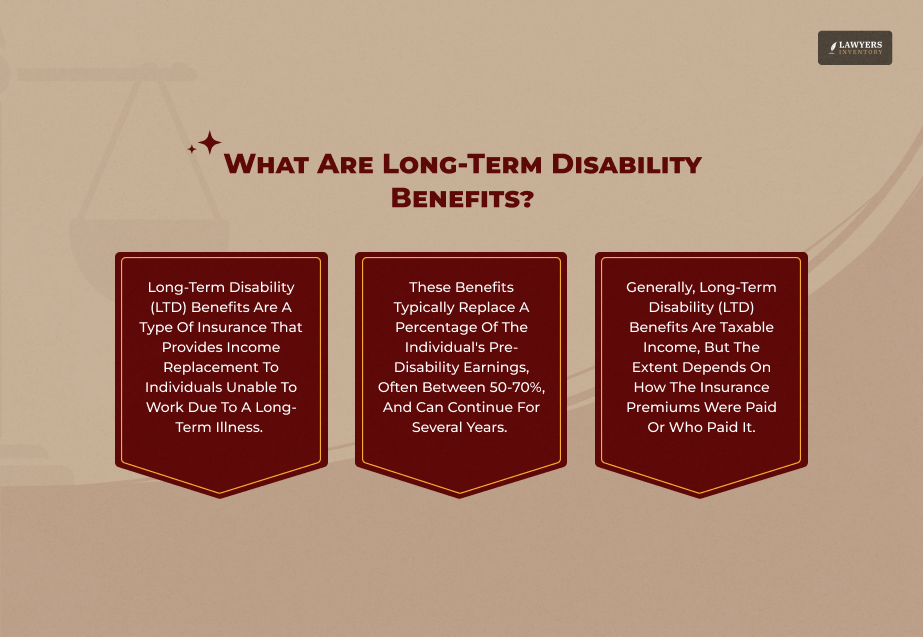

Now, I know that it’s scary. And that’s not just because of the health issue. Rather, it is because you might not get a paycheck. That’s where Long-Term Disability (LTD) benefits come in.

These are payments that help you cover bills when you can’t work for a long time. But here’s the twist: Many people think these payments are always tax-free.

That’s not always true.

Irrespective of the fact whether your LTD benefits are taxable depends on a few things, especially who paid for your insurance premiums and how they paid.

Hi. In today’s blog, I will talk about how and when Long-Term Disability benefits are taxable. Additionally, I will also tell you some of the best tips that you can use to ensure that you are able to save that money!

So, if this is something that you are searching for, then you have come to the right place. Therefore, keep on reading till the end and thank me later…

Is Long Term Disability Taxable In The United States?

The regulations enumerating who is liable for federal tax with respect to LTD or STD income are conditional upon the following:

- Who carried out the payment of premiums— the employee or the employer?

- What was the nature of the method of payment for premiums— were they pre-tax or post-tax?

Basically, the tax rules go as follows: if the employer paid for the premiums, then the income component that the employee receives from the disability is subject to taxation. Thus, the employee shall be liable for income tax.

Likewise, if the premiums were paid with pre-tax money, the disability income also is subject to tax.

Nonetheless, in the event that the premiums are covered with after-tax money, the payments received from the disability income are not subject to federal taxes.

To elucidate, the tax could be either paid by the IRS upfront (before premium payment) or upon receiving the disability check (disability benefit).

Long term disability income plans can be employer-paid, same as STD. When the employer finances the premium, the payments during the period of disability will be considered as taxable income.

In contrast to that, in case you made the payment for part or all of the premium from your own after-tax money, that part of the income will not be covered by federal tax.

Let me now explain in detail about when is long term disability taxable!

Who Paid the Premiums?

This is the biggest rule: The taxability of your LTD benefits depends on who paid the insurance premiums.

There are two types of payments:

After-Tax Premiums

- You paid for the insurance using your own money, and you were already taxed on that money.

- Example: You earn $1000, taxes are taken out, and you use your leftover money to pay for insurance.

Pre-Tax Premiums

- Your employer paid for the insurance or took the money from your paycheck before taxes were applied.

- Example: You earn $1000, but before taxes are taken, $50 is used to pay your insurance. You’re not taxed on that $50, but you’ll pay taxes later on the benefits.

| Who Paid for LTD? | Were Taxes Paid on the Premium? | Are the Benefits Taxable? |

| Employee (After-Tax) | Yes | No |

| Employer (Pre-Tax) | No | Yes |

| Both (Mixed) | Partially | Partially |

Why does the IRS do this? It’s to avoid double taxation. If you already paid taxes once, you shouldn’t pay again. But if you never paid taxes on that money, the IRS wants its share.

Detailed Scenarios of Federal Taxability

Let’s walk through some common situations to make this even easier:

Scenario 1: Employer Paid All Premiums (Pre-Tax)

- Rule: The full benefit is taxable.

- Why: You never paid taxes on the money your boss used to buy your insurance.

Example:

- Monthly LTD benefit: $5,000.

- All premiums paid by employer.

- Result: You must report $5,000 as taxable income.

Scenario 2: You Paid All Premiums (After-Tax)

- Rule: The benefit is tax-free.

- Why: You used your own, already-taxed money to buy the coverage.

Example:

- Monthly LTD benefit: $5,000

- All premiums paid by you (after-tax)

- Result: $0 is taxable

Scenario 3: Mixed Payments

- Rule: Only the employer’s share of the premiums determines how much is taxable.

- Calculation: If the employer paid 70%, then 70% of the benefits are taxable.

Example:

- Monthly benefit: $5,000

- Employer paid 70%, employee paid 30%

- Taxable part: 70% of $5,000 = $3,500

- Tax-free part: 30% of $5,000 = $1,500

Here’s What Happens When You Are Self-Employed

• If you’re self-employed, you usually pay premiums with after-tax dollars.

• That means LTD benefits are usually tax-free.

• However, if you deducted those premiums as a business expense, then the benefits become taxable.

Reporting LTD Benefits on Your Tax Return

Let’s say you’re getting LTD benefits. How do you tell the IRS?

As we all know, the Internal Revenue Service (IRS) is the primary tax authority in the U.S. It is worth noting that the agency has provided guidance on whether individuals are required to pay taxes on disability benefits received from long-term disability insurance.

It says that the most important point to consider is the question of who paid the premiums— was it you, your employer, or did you both share the expense?

Briefly put, according to the government, if the employer issues you the insurance policy as a benefit, then the money you get out of it shall be fully taxable.

The coverage you get by using money after the tax deduction, which is post-tax dollars, will normally not be subject to tax on the monthly payment.

Besides that, the IRS carries the message loud and clear that any money that the employer gives to the worker will be considered as income that is subject to the tax if the worker has to stay at home due to illness or injury, and it should therefore be reported as such.

Here’s how you can report tax returns:

You Might Get One of These Forms:

- W-2: If your employer paid the benefits directly

- 1099-MISC: Most common form if an insurance company paid you

- 1099-R: If LTD benefits came from a retirement plan

Where to Report It:

- On Schedule 1 (Form 1040) under “Other Income”

- Or directly on Form 1040, depending on the form type

Role of Insurance Company:

- They decide what part of your benefits is taxable, based on their records

- Always check their numbers; mistakes can happen

Don’t Forget Taxes

If your benefits are taxable, you may:

• Need to adjust your tax withholdings

• Or make quarterly tax payments to avoid penalties

Special Considerations & Other Benefits

Yes, just in case you were wondering, there are special considerations related to LTD benefits. Here’s what you need to know:

Lump Sums or Back Pay

- If you win your case and get a big check, that money is taxed based on the original rule: who paid the premiums.

- But large lump sums can bump you into a higher tax bracket for that year.

- Tip: Talk to a tax pro about spreading the income across multiple years.

What About State Taxes?

Each state has its own rules. For instance, take a look at this chart:

| State | Taxes LTD? |

| California | Yes |

| Florida | No (No income tax) |

| New York | Yes |

| Texas | No (No income tax) |

So, it is best that you always check with your state tax office.

Other Benefits

Here are some additional benefits that you need to know about:

- Workers’ Compensation: This one is never taxable. It’s money for injuries on the job.

- Social Security Disability (SSDI): Sometimes taxable. It is generally, based on “provisional income” (your income + ½ SSDI + other tax-free income). Also, LTD policies often reduce your benefit if you get SSDI, so only the LTD amount you get is taxed.

- Veterans’ Disability: Always 100% tax-free

- Long-Term Care Insurance: Not LTD. Usually tax-free up to certain daily limits.

- Other Government Help: If your LTD income is taxable, it might affect your eligibility for programs like Medicaid, SNAP (food stamps), and Housing help.

Things To Keep In Mind About Long-Term Disability Benefits

Now that you are aware of what Long-Term Disability Benefits are, and how you can deal with the taxation, let me tell you a few things that you MUST (at all cost) keep in mind:

Common Mistakes

- Thinking all LTD benefits are tax-free

- Losing paperwork about who paid premiums

- Forgetting to pay quarterly taxes on taxable benefits

Helpful Tax Credits/Deductions

- Medical Expense Deduction: If your medical costs are high (more than 7.5% of your income)

- Credit for the Elderly or Disabled: You might qualify if your income is low and you’re permanently disabled

Retirement & Disability

If you’re permanently disabled, you can take early withdrawals from IRAs/401(k)s without a penalty (but still pay income tax). Additionally, if you still have earned income, you can contribute to IRAs

What If Your LTD Is Approved After a Delay?

Yes, this is also a possibility. And what can you do in such a situation?

Generally, in that case, you may get a big lump sum. However, here’s what you need to know: Even though you waited months or years, it counts as income for the year you receive it.

Again, plan carefully to avoid big tax bills!

So, Are Long-Term Disability Benefits Taxable?

Long term disability benefits might be the only source of income in difficult times. However, with regards to taxes, the situation is not always straightforward.

The most important rule to keep in mind is: Who and in what way covered your insurance decide if your LTD benefits are subject to tax.

Additionally, you need not tackle this alone. Your LTD case is unique. The best move? Talk to:

- A tax professional

- A financial planner

- Or a disability lawyer

Having correct knowledge, keeping good records and getting help from experts make it possible to manage your money well even in difficult times.

Leave A Reply

Slip And Fall Lawyer: Famous Cases And Expert Hiring Tips

Read More

Attorney Kenneth Powell: Fighting For Justice In Personal Injury Cases

Read More

Attorney Josh Bonnici On The Responsibility Of Handling Serious Personal Injury Cases

Read More

0 Reply

No comments yet.