Today’s topic: Is National Debt Relief legit?

For the longest time, I have closely tracked the credit market. Many people face extreme financial strain from mounting debt. Consequently, they become vulnerable to misleading marketing ploys.

Therefore, I avoid surface-level promotional claims in this report. Instead, I base this evaluation on verified datasets and Federal Trade Commission (FTC) parameters.

Our primary goal is to analyze third-party debt settlement frameworks objectively. Furthermore, we will highlight the strategic risks and hidden program costs. As a result, you can make a safe and informed decision.

Overview: What Is National Debt Relief?

National Debt Relief started in 2009. Since then, the company has grown into a massive debt settlement operation.

In fact, it has guided more than 1.3 million people through its program. However, the company does not offer fixed-rate consolidation loans.

Additionally, it does not function as a non-profit credit counseling agency. Instead, the company focuses entirely on a backend principal negotiation model.

According to data from the American Association for Debt Resolution (AADR), debt clearers assist over 1.24 million consumers annually. For instance, these companies secure an aggregate of $1.8 billion in total savings. (Source: Credible)

National Debt Relief manages an enormous market share in this ecosystem. Specifically, they have settled more than $10 billion in gross debt over their operational history.

How Does National Debt Relief Work?

The company uses a structured pipeline to target banks and collection firms. Here is how the pipeline looks:

- Free Consultation.

- Underwriting and Soft Credit Check.

- Stop Paying Creditors.

- Build FDIC Escrow Funds.

- NDR Negotiates Settlement

- You Approve Offer

- NDR Collects Fee.

As per the official site of National Debt Relief, here are the steps in detail:

Analysis And Soft Pull:

First, a certified debt specialist evaluates your finances. The specialist runs a soft credit check. Fortunately, this check does not lower your FICO score. Afterward, they generate a personalized savings quote.

The Escrow Foundation:

Next, your portfolio must clear corporate underwriting. Once enrolled, National Debt Relief opens a secured escrow savings account in your name.

This account is held at an independent bank. However, managing this repository carries a one-time setup fee of $9.00. Additionally, you will pay a standard monthly maintenance fee of $9.85.

Payment Redirection:

Afterward, you must freeze all payments going directly to your creditors. Instead, you redirect those funds into your new escrow account. You can choose a bi-weekly, semi-monthly, or monthly draft schedule.

The Negotiation Window:

Meanwhile, your accounts slip into deep default. National Debt Relief uses your growing escrow balance as leverage.

Consequently, they offer creditors a lump-sum payout for less than the full balance. Typically, the first settlement offer materializes 4 to 6 months after enrollment.

Program Completion:

Finally, graduates who maintain their monthly escrow deposits usually complete the program within a 24 to 48-month window.

Is National Debt Relief Legit?

Yes, National Debt Relief is an entirely legitimate corporation. For example, the company is fully accredited by the Better Business Bureau (BBB) with an A+ rating.

Furthermore, it is recognized as a USA Today Trusted Brand. It also maintains strong verification scores across independent consumer tracking platforms:

| Reputable Platform | Total Volume | Star Rating | Verification Notes |

| Trustpilot | 41,000+ Historic | 4.7 / 5.0 | Clean profile; less than 3% of entries are below 3 stars. |

| ConsumerAffairs | 56,000+ Historic | 4.9 / 5.0 | High marks for customer service empathy. |

| Better Business Bureau | 5,372 Active | 4.8 / 5.0 | 410 complaints logged; 88 formally resolved. |

However, legitimacy does not guarantee safety. Legally, the company operates within the boundaries of the FTC’s Telemarketing Sales Rule (TSR) amendments. Under these rules, debt relief firms cannot charge advance fees. (Source: Lexology)

Therefore, they are barred from taking a commission until they successfully reduce a debt. You must also sign the settlement agreement first.

Their performance service fee ranges from 15% to 25% of the enrolled debt. For example, if you enroll a $20,000 credit card balance, your final cost will range from $3,000 to $5,000.

Consequently, this fee is collected proportionally only as individual lines of credit are resolved.

Contextualizing The Legal Risk: The Debt Court Crisis

Now that you know the answer to “Is National Debt Relief legit?” let’s talk about something most people often worry about – the legal risks.

To accurately evaluate this trend, we must look at modern U.S. civil courts. Many individuals seek out debt settlement to avoid lawsuits.

According to research by The Pew Charitable Trusts, debt collection lawsuits dominate state civil court dockets. For instance, at least 2.5 million civil debt lawsuits are filed annually across the United States. (Source: Forbes)

Furthermore, Pew’s analytics show that more than 1 in 5 Americans hold a balance in active collections.

In addition, 1 in 20 citizens faced a civil collection lawsuit in a single year across multiple analyzed states.

Therefore, ignoring your debt carries independent legal risk. This threat frequently drives consumers toward third-party arbitration.

Program Qualification And Eligible Underwriting

National Debt Relief enforces strict underwriting rules. To qualify for an evaluation, you must meet these baseline metrics:

- Minimum Debt Threshold: First, you must carry a minimum of $7,500 in qualifying debt.

- Verifiable Financial Hardship: Next, you must document a severe economic hardship. Examples include job loss, medical emergencies, or divorce.

- The Referral Safety Net: However, if you do not qualify for settlement, the company offers an alternative. They automatically refer individuals to partners like Reach Financial. This partner offers fixed-rate debt consolidation loans ranging from $3,500 to $40,000.

Eligible vs. Ineligible Balance Classifications

The architecture of debt settlement only permits unsecured liabilities. Consequently, secured items are structurally excluded:

| Eligible Unsecured Debt | Ineligible Debt Types |

| Credit cards (retail, bank, gas cards) | Mortgages and home equity loans (HELOCs) |

| Unsecured personal installment loans | Financing, leases, or loans for vehicles |

| Private bank loans and fees | Outstanding federal, state, or local back taxes |

| Vehicle repossession deficiencies | Court-ordered child support payments |

| Delinquent lines of credit and collection accounts | Current utility or active cell phone bills |

| Overdue back rent payments | Speeding tickets, legal fines, and court penalties |

| Medical and vet bills (over $500) | Active insurance policy balances |

| Unsecured business debts | Criminal bail bonds |

| Certain private student loans | Federal student loans |

The Dark Side Of Debt Settlement: Common Pitfalls

While the company maintains clean legal compliance, consumer forums like Reddit illustrate a different reality. Enrolled clients frequently experience distinct operational roadblocks midway through their plans:

The “Verbal Agreement” Trap

Sales representatives regularly offer verbal assurances during phone calls. For example, they might promise that a fixed monthly payment of $700 will resolve your entire debt load.

However, the written contract contains language that supersedes these spoken claims. Therefore, if negotiations stall because your escrow builds too slowly, account managers will demand extra payments.

Sidelined Accounts And The “Sallie Mae” Protocol

Certain creditors are notoriously aggressive and rigid. For instance, private student loan servicers like Sallie Mae rarely cooperate.

Credit card companies operate with high profit margins, so they easily write off partial losses. Conversely, private student loan entities hold tightly to fixed installment assets.

Consequently, if a creditor rejects a settlement offer, National Debt Relief will drop that account from your program.

Legally, this drops you back into active collections. As a result, you become individually responsible for defending against lawsuits.

Lack Of Written Communication

When problems escalate, customer service agents often avoid email. Instead, they prefer undocumented phone calls.

However, you have the right to request documentation in writing. If a company repeatedly avoids providing answers via email, it is usually a tactic to limit your paper trail.

Macro-Economic Trends: The “Litigation Probability Index”

When analyzing credit portfolios, you must look closely at the specific institutions holding your balances. Not all debts behave similarly during an intentional default phase:

- High Settlement / Low Litigation Probability: Large national credit card issuers (e.g., Chase, Capital One) and third-party debt buyers (e.g., Midland Credit Management). These entities manage millions of delinquent accounts. Therefore, they routinely choose systematic settlement percentages over paying high legal fees for court lawsuits.

- Low Settlement / High Litigation Probability: Local credit unions, local medical systems, and secondary asset financing firms. These institutions hold tightly to their documentation. Consequently, they are organized to file collection lawsuits quickly to secure wage garnishments.

Also, where you live can have a profound effect on your legal safety. States set a limited shelf life for creditors’ ability to litigate against you. The time limits set by statutes of limitations can be anywhere from three to ten years.

For example, let’s say there is a state with a short 3-year statute. If you were living in that state, 24 months of nonpayment would put your creditors between a rock and a hard place.

As a result, they will either allow the debt to expire or sue you right away. Your risk of being sued for mid-program skyrockets.

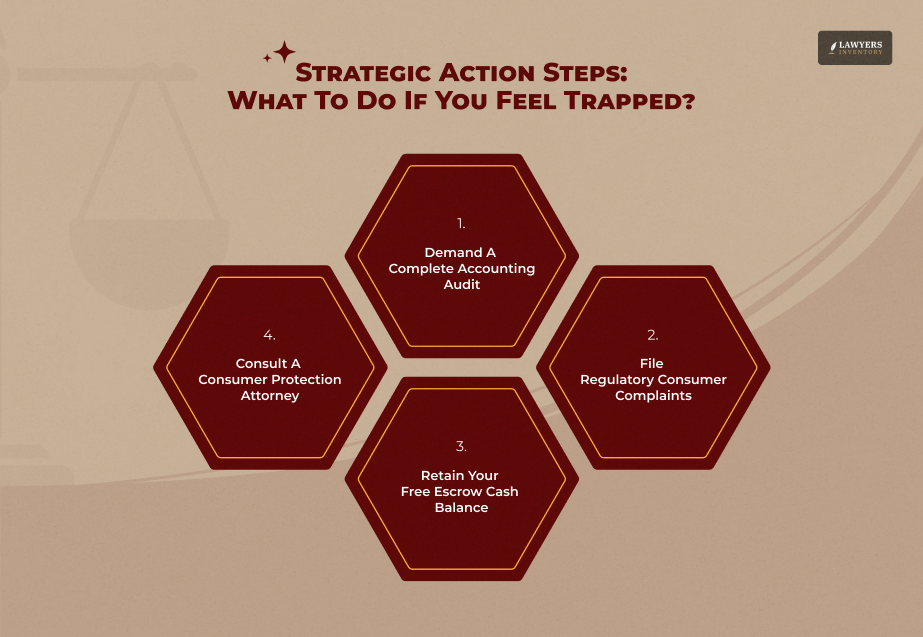

Strategic Action Steps: What To Do If You Feel Trapped?

If you are already enrolled and find yourself facing unexpected issues, you must transition from a passive client to an active self-advocate:

Demand A Complete Accounting Audit:

Formally request a written ledger of your escrow account. You need to verify exactly how much of your funds have been distributed to creditors versus how much has been taken out as corporate service fees.

File Regulatory Consumer Complaints:

If you have been misled by unverified verbal promises, log into detailed consumer complaints. You can submit these directly to the Consumer Financial Protection Bureau (CFPB) and your state’s Attorney General. Consequently, these complaints force a formal response from the company.

Retain Your Free Escrow Cash Balance:

Legally, the money in your dedicated escrow account belongs to you until a settlement is executed. Therefore, if you choose to terminate the program, you have the right to pull out your remaining cash.

Consult A Consumer Protection Attorney:

If you’ve had an account closed and you get sued for collection, talk to a local consumer protection attorney quickly.

They will be able to examine your contract to see if it’s been breached. Also, they will be able to advise whether bankruptcy is wise to prevent creditor action.

Strategic Comparison Of Legal Alternatives

If the risks of debt settlement feel too volatile for your financial situation, you have other legal frameworks to explore.

Non-Profit Credit Counseling (DMPs)

Organizations like the National Foundation for Credit Counseling (NFCC) build Debt Management Plans (DMPs). They do not cut your principal balance.

Instead, they work with creditors to slash interest rates to near 0% and waive ongoing penalty fees.

Consequently, your accounts stay open and in good standing, saving your credit score while combining your bills into one monthly payment.

DIY Debt Repayment Strategies

If your income allows you to pay more than the bare minimums, you can manage your own recovery without third-party fees:

- Debt Snowball: Pay off your smallest individual debts first. This builds psychological momentum and reduces the total number of open accounts quickly.

- Debt Avalanche: Target your highest-interest balances first. Consequently, this method saves you the maximum amount of money on compounding interest over time.

Structured Debt Consolidation Loans

If you still maintain fair to excellent credit, you can take out a fixed-rate personal consolidation loan. This wipes out high-interest credit cards instantly.

Furthermore, it transforms multiple scattered bills into one predictable monthly payment and improves your credit score.

Zero-Interest Balance Transfer Cards

Transferring these balances to a new credit card with an introductory 0% APR period can save you hundreds of dollars.

During the initial term period, you will be required to make a small upfront transfer fee (3% to 5%). Yet, every penny of this transfer fee goes directly toward your principal during the introductory period.

Competitor Comparison: Freedom Debt Relief vs. National Debt Relief

Comparing top-tier providers is essential. While both companies offer identical qualification criteria, their pricing structures diverge slightly. Freedom Debt Relief establishes a sliding fee scale from 15% to 25% based on state laws.

Conversely, National Debt Relief consistently trends directly toward a flat 25% fee setup. Therefore, Freedom can potentially be more cost-effective depending on your state.

Legal Bankruptcy Filings

Consulting a licensed consumer bankruptcy lawyer gives you court-mandated federal protections that private companies cannot match.

- Chapter 7 Bankruptcy.

- Chapter 13 Bankruptcy.

Both bankruptcy paths instantly trigger a federal automatic stay. Legally, this block stops creditors from calling you, suing you, or executing garnishments immediately.

Summary Comparison Table

| Operational Feature | National Debt Relief (Settlement) | Non-Profit DMP (Counseling) | Debt Consolidation Loan | Chapter 7 Bankruptcy |

| Principal Reduction | Yes, averages 25% net savings. | No, full principal must be paid. | No, balance is simply shifted. | Yes, eliminated completely. |

| Impact on Credit Score | Severe, immediate short-term drop. | Mild, occasionally positive over time. | Positive, lowers utilization quickly. | Severe, remains on report for 10 years. |

| Protection Against Suits | None; lenders retain the right to sue. | Voluntary; based on creditor agreements. | None; standard loan contract rules apply. | Immediate automatic stay stops legal actions. |

| IRS Tax Implications | Forgiven balances are taxed as income. | None; no debt is forgiven. | None. | Discharged debt is entirely tax-exempt. |

Core Verdict: Is National Debt Relief Legit?

National Debt Relief provides an entirely legitimate, legally compliant debt settlement service under the strict enforcement of the Federal Trade Commission’s Telemarketing Sales Rules.

However, its strategic reliance on consumer delinquency means applicants face substantial risks regarding immediate credit damage, compounding balances, and collection lawsuits that must be weighed against their potential 25% net principal savings.

Read Also:

- Is Super.Com Legit Or A Scam? What Does Consumer Protection Laws Say?

- Is Superbox Legal? Things You Really Need To Know For Complete Safety

- The Legality Of The HidingMe VPN: Should Law Firms Use It?

Leave A Reply

Hung Jury vs. Mistrial: What Is The Difference And Why It Matters

Read More

NarodniyDimUkraina: An Overview Of The Kyiv-Based Brand Preserving Ukrainian Craftsmanship

Read More

What Is A Mistrial? Legal Definition, Causes, And What Happens Next

Read More

What Is A Sequestered Jury? Legal Definition, Process, And Everything You Need To Know

Read More

What Is A Hung Jury? Legal Definition, Causes, And What Happens Next

Read More

0 Reply

No comments yet.