Mr. Cooper is one of the largest home loan servicers in the United States. Previously, the company operated under the name Nationstar Mortgage. Today, it manages millions of residential mortgages.

However, the company has faced massive regulatory penalties and private class actions over the years. These legal challenges involve predatory fee models, severe mortgage servicing failures, and major data breach liabilities.

Consequently, homeowners must understand these distinct legal actions to protect their financial equity and digital privacy.

If you want to know more about Mr. Cooper Class Action Lawsuit, keep reading!

Quick Answer: About Mr. Cooper Class Action Lawsuit

Mr. Cooper (Nationstar Mortgage) is navigating multiple legal actions, primarily centered on a 2023 data breach affecting 14.7 million customers and lawsuits regarding illegal pay-to-pay convenience fees. Various multi-million dollar settlements have been reached, alongside a significant government enforcement action regarding loan handling. Affected customers should check their mail notices for specific case numbers and deadlines to claim payouts.

The $91.2 Million Government Settlement On Mr. Cooper Class Action Lawsuit

In December 2020, state and federal regulators finished a massive enforcement action against Nationstar Mortgage LLC (doing business as Mr. Cooper). Specifically, government attorneys filed two parallel cases in the U.S. District Court for the District of Columbia:

- The State of Alabama, et al. v. Nationstar Mortgage LLC d/b/a Mr. Cooper (Case No. 1:20-cv-03551)

- Bureau of Consumer Financial Protection v. Nationstar Mortgage LLC (Case No. 1:20-cv-03550)

The Legal Allegations

First, the Consumer Financial Protection Bureau (CFPB) and state banking regulators launched a multi-year investigation. [Source: Consumer Finance]

As a result, authorities uncovered systemic misconduct and abusive mortgage servicing practices between 2012 and 2015.

Ultimately, Nationstar violated multiple consumer protection laws, including RESPA and the Homeowners Protection Act.

During the investigation, regulators found several major operational abuses:

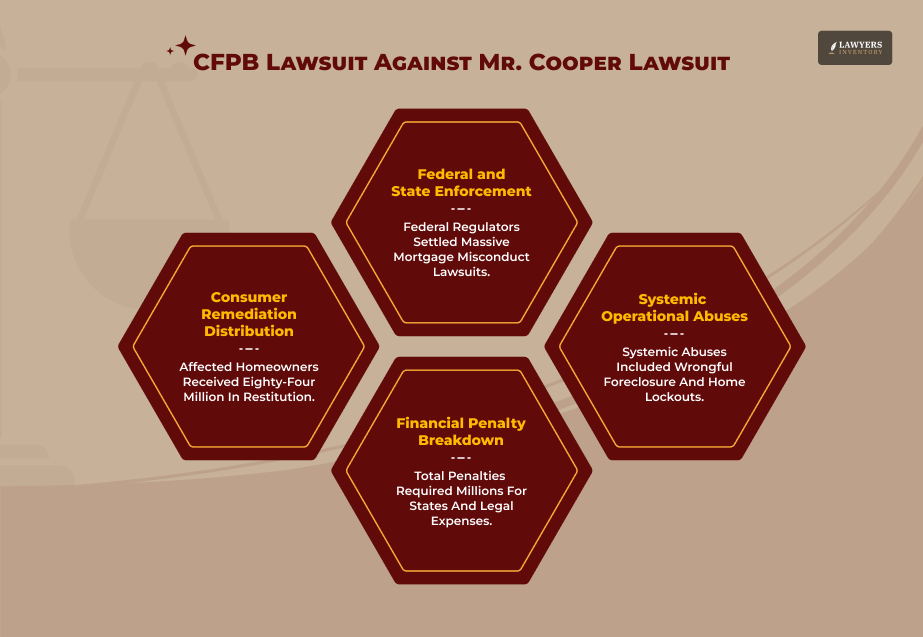

- Wrongful Foreclosures: Nationstar routinely foreclosed on homes while homeowners were still waiting for loan modification choices. In fact, the company even sold properties belonging to borrowers who were actively paying on agreed modifications.

- Deceptive Account Changes: Furthermore, the company failed to honor permanent loan modification agreements. Instead, it unlawfully increased monthly loan payments on fixed-rate accounts.

- Escrow Mismanagement: Additionally, the servicer failed to analyze escrow accounts properly and missed property tax deadlines. The company also created fake account shortages for borrowers in bankruptcy and tried to collect the money without court permission.

- PMI Overcharges: Moreover, Nationstar failed to remove private mortgage insurance (PMI) on time, which forced borrowers to pay unnecessary premiums.

- Lockout Violations: Finally, the company hired third-party vendors who falsely marked occupied homes as “vacant.” Consequently, these agents unlawfully changed the locks and trapped residents outside their own homes.

Payout Structure

Because of these violations, the court ordered a total financial package of $91,255,843. [Source: Top Class Actions]

This total included:

- $1.5 million CFPB penalty.

- $1.2 million to participating states.

- $3.86 million in legal fees.

Meanwhile, the remaining $84 million went directly to consumer remediation.

As part of this deal, the 50 state Attorneys General managed a specific $5.8 million joint settlement. This fund split affected consumers into two target groups:

- The Service Transfer Population: This group includes borrowers whose loans moved in bulk to Nationstar between 2011 and 2017. Because of servicer errors, these accounts fell delinquent within 90 days of the transfer, resulting in foreclosure. Therefore, cash payouts helped remedy the financial and tax damages from those forced sales.

- The Property Preservation Population: This group includes homeowners who faced unlawful lockouts by Nationstar agents between 2011 and 2017. As a result, cash awards reimbursed these victims for their emergency expenses and distress.

RECENT DEADLINE NOTICE

The official claims process for this multi-state settlement has ended. [Source: NationalNationstarSettlement.com]

The administrator mailed information packets and claim forms to eligible members in late 2024. Ultimately, the hard deadline to submit a claim form was March 3, 2025.

The Convenience Fee Mr. Cooper Class Action Lawsuit

In addition to government action, private attorneys targeted Mr. Cooper’s automated fee structures.

The Predatory Fee Model

Plaintiffs in multiple class actions alleged that Mr. Cooper penalized borrowers for making standard monthly payments.

Specifically, the company charged an extra convenience fee – usually $5 to $15 per transaction – whenever a borrower paid their mortgage online or over the phone. [Source: Top Class Actions]

Subsequently, the lawsuits argued that these “pay-to-pay” charges violated state debt collection rules and breached mortgage contracts. [Source: National Mortgage News]

Because the original loan notes never authorized these transaction fees, the courts deemed the practice unlawful.

The Resolution

Eventually, Mr. Cooper resolved this litigation by agreeing to a $10 million settlement. Besides providing cash payouts to affected members, this case set a major industry precedent.

Now, national mortgage servicers cannot charge transaction fees on basic payment portals unless the original contract explicitly allows it.

The 2023 Cyberattack Data Breach Litigation

The most recent legal battle centers on a massive cybersecurity failure that occurred in late 2023.

The Breach And Harm Allegations

On October 31, 2023, Mr. Cooper was the victim of a very serious cybercrime.

As a result, the company shut down its transactional systems for more than a week, preventing millions of homeowners from making their mortgage payments.

Next, an investigation showed that the hackers had extracted personal information of approximately 15 million current and former customers.

The compromised data consisted of names, dates of birth, telephone numbers, residential addresses, Social Security numbers, as well as bank details.

Therefore, plaintiffs filed a consolidated class action called In re: Mr. Cooper Group Inc. Data Security Litigation in the U.S. District Court for the Northern District of Texas. [Source: National Mortgage Professional]

The lawsuit alleges that the company ignored repeated hacking attempts and failed to implement basic data security safeguards.

Key Court Ruling

Recently, Chief District Judge David Godbey issued a pivotal ruling that allowed the core parts of this lawsuit to move forward. [Source: Bloomberg Law]

The court evaluated Mr. Cooper’s motion to dismiss and established these parameters:

- Legal Standing Allowed: First, the court ruled that exposing sensitive data on the dark web causes concrete injury. Thus, the judge dismissed Mr. Cooper’s argument that the consumer risk was merely speculative.

- Negligence Claims Stand: Second, the court preserved the plaintiffs’ claims for negligence and breach of implied contract. The judge noted that companies have an implied obligation to safeguard customer data, even without a signed privacy agreement.

- Dismissed Claims: However, the judge dismissed allegations of express-contract breaches and invasion of privacy, finding them unsupported by Texas law.

- Deferred Issues: Meanwhile, the court deferred structural arguments regarding state-specific privacy laws to upcoming class-certification proceedings.

The Strategic Corporate Impact

Importantly, this active litigation unfolds during a massive corporate shakeup. Rocket Companies (the parent company of Rocket Mortgage) completed a historic $14.2 billion acquisition of Mr. Cooper Group.

Although this merger creates an industry giant, the unresolved data breach lawsuit remains a major liability.

Under standard corporate merger rules, Rocket Companies inherits Mr. Cooper’s outstanding legal liabilities, which ties the final data breach resolution directly to the new merged entity.

Consumer Protection Protocol For Homeowners

These multi-million dollar outcomes prove that homeowners have strong legal tools to fight back. Therefore, if you spot unexplained fees or billing errors on your mortgage statements, follow these protection steps:

Submit A Qualified Written Request (QWR):

Under RESPA guidelines, you can mail a formal, physical error-assertion letter to your servicer. Consequently, the company must acknowledge receipt within 5 business days and resolve the issue within 30 business days.

File A Regulatory Escalation:

If your loan servicer ignores your letter, file an official dispute directly with the Consumer Financial Protection Bureau (CFPB) and your state’s Attorney General.

Retain Legal Counsel:

For severe financial damages, look for a consumer protection attorney who specializes in RESPA and the Fair Debt Collection Practices Act (FDCPA).

Generally, reputable consumer law firms operate on a contingency fee structure, meaning you pay nothing upfront unless they win a settlement for you.

Read Also:

- Smoothstack Lawsuit: Beware of Unlawful Wage Scheme and Employment Contracts

- 72 Sold Lawsuit Exposed the Deceptive Marketing Strategies of Real Estate Agents!

- Kennedy Funding Lawsuit and the Exploitation of Arkansas Statute of Frauds

Leave A Reply

Understanding What Does Under Contract Mean In Real Estate

Read More

Texas Built Construction Lawsuit Explained: Rights, Remedies, And Legal Truths

Read More

Understanding The Lady Bird Deed: What Is It & How Is It Better?

Read More

Is Section 8 Getting Cut Off: Answering The Most Asked!

Read More

0 Reply

No comments yet.