Quick Answer

New York enacted the pied-à-terre tax on 28 May 2026, as part of its FY2026-2027 (budget of $268 billion). The annual levy applies to luxury residential real estate in New York City that is not the primary residence of the property owner. It is expected to raise at least $500 million per year. New York City's deficit runs at $5.4 billion in FY2027 and is expected to grow to $10 billion and beyond in later years. The tax is a meaningful revenue contribution - but on its own, it does not close the deficit.

What Is The Pied-À-Terre Tax?

On May 27, 2026, the New York State Legislature passed the pied-à-terre tax as part of the 2026-2027 state budget.

This tax is effective for NYC fiscal years starting July 1, 2026. It applies to luxury second-home property owned by non-NYC resident primary owners.

From what I read on several sources, including Steptoe, the new law will expire on 30 June 2031 unless it is extended.

The tax was first announced by New York Governor Kathy Hokul on April 15, 2026, to help NYC Mayor Zohran Mamdani close the NYC budget deficit.

Steptoe predicts the project will create approximately $500 million annually of recurring revenue for the city and will impact about 10,000 single-family homes, co-ops, and condos citywide.

The concept is not new.

Versions of this legislation have been introduced in every session since 2019, dying in committee each time. What is different today is that the governor is driving it rather than observing from a distance. [Source: Brandonmason]

Governor Hochul specifically cited supertall towers along Billionaires’ Row – properties worth upwards of $100 million that have never been occupied – as the clearest illustration of the problem the tax addresses.

Who Does Pied-À-Terre Tax Apply To?

The tax applies only to non-primary residences that fall within the definition of “covered property.” [Source: Cole Schotz] These include:

- One- to three-family homes valued at $5 million or more.

- Residential co-op units valued at $1 million or more.

- Residential condominium units valued at $1 million or more.

An important distinction: the dollar thresholds refer to market value, not assessed value.

New York City’s assessed values are deliberately depressed for residential property [Source: Reed Corporation]. This is why the legislation uses market value as the operative measure for single-family homes while applying assessed value thresholds to condos and co-ops, where DOF assessments have historically run lower than actual market value.

According to analysis by EisnerAmper, if the owner already pays New York City personal income tax as a resident, the property is exempt regardless of value. This is the principal exemption. Primary residence is the central determining test.

What Are The Tax Rates?

The legislation operates in two phases.

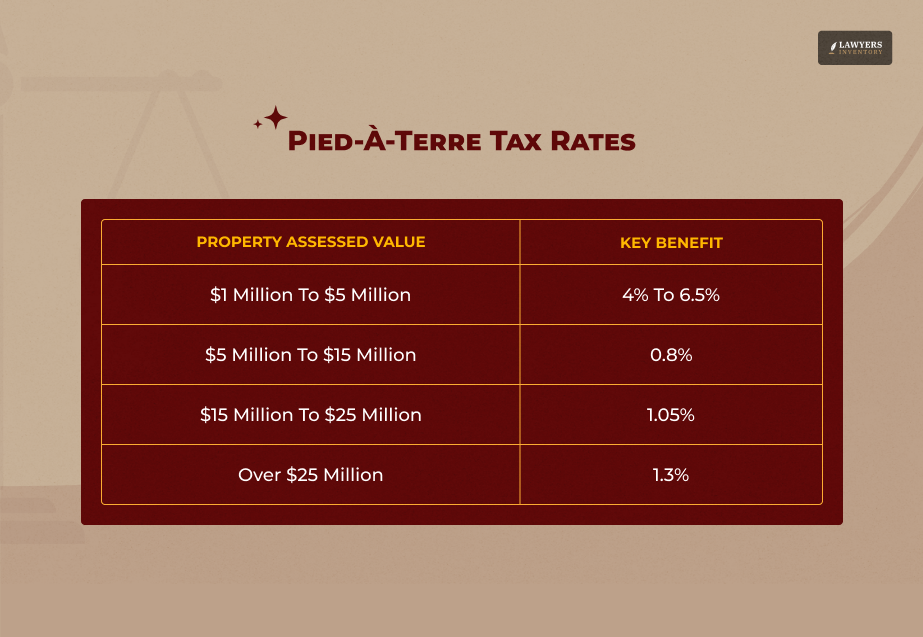

Phase 1 (July 1, 2026 – June 30, 2028)

From the expert opinions I found at Dechert, during Phase 1, the surcharge applies to condos and co-ops with an assessed value of $1 million or more at the following rates:

- 4% for properties with an assessed value between $1 million and $3 million

- 5.25% for properties with an assessed value between $3 million and $5 million.

One- to three-family homes valued at $5 million or more will be taxed between 0.8% and 1.3%, depending on DOF assessed value.

Phase 2 (July 1, 2028 – June 30, 2031)

Next, beginning July 1, 2028, the tax will shift to a new valuation model that applies the same rates to all one- to three-family homes, condos and co-ops valued at $5 million or more.

Under this model, one- to three-family homes will be valued based on their current DOF assessed value. On the other hand, condos and co-ops will be valued based on actual sales of comparable units.

As per my analysis, phase 2 represents a structural overhaul of how the NYC DOF values co-ops and condominiums – a process that has been deferred for decades.

How Is Primary Residence Determined?

The Department of Finance will consider documents such as tax returns and lease agreements, in addition to whether the owner or an immediate family member occupied the property for a majority of days during a calendar year.

New York’s Department of Finance will notify owners of properties subject to the tax no later than August 30, 2026.

After which time owners may contest such determination by submitting proof of primary residence, such as the covered owner’s tax return identifying the property as a permanent home address or a qualifying lease agreement.

The Department has six years to audit any certification or documentation submitted. Additionally, the surcharge remains valid even if the Department fails to satisfy its notice obligation.

A Critical Planning Note:

An individual who owns a high-value residential property in New York City may consider using the property as a “primary residence” to avoid the surcharge. However, doing so will require the taxpayer to be subject to New York State and New York City personal income tax, which otherwise applies only to City residents. For many high-net-worth non-residents, this trade-off makes declaring primary residency unattractive.

How and When Is It Paid?

The surcharge will be added to the covered property’s statement of account and will be administered and enforced in the same manner as real property taxes, except that any abatement, credit, or exemption authorized by law will not apply to the surcharge.

For the fiscal year beginning July 1, 2026, the surcharge will be due and payable on January 1, 2027.

Beginning in the 2026-2027 tax year, the surcharge will be levied alongside real property taxes and enforced through similar collection mechanisms, including liens and foreclosure proceedings.

The NYC DOF will have audit authority extending up to six years with regard to documentation submitted under the new law.

Can Pied-À-Terre Tax Actually Close The Budget Gap?

This is the central question – and the honest answer is: not alone.

New York City collected $81.4 billion in total tax revenue in fiscal year 2025. The proposed pied-à-terre tax adds $500 million, which is roughly one-tenth of a budget gap that currently stands at $5.4 billion for fiscal year 2027, and is projected to reach $10 billion or more in subsequent years. [Source: Brandonmason]

The tax is therefore a meaningful contribution – roughly 9% of the current gap – but not a structural solution.

It is best understood as one tool in a broader fiscal strategy, which the FY2027 budget acknowledges by pairing the pied-à-terre surcharge with $1.5 billion in additional state aid for the city.

There is also a behavioral response risk.

Vancouver introduced its Empty Homes Tax in 2017 at a rate of 1% of the assessed property value. The city then increased this rate to 3% by 2021.

Consequently, many property owners changed their behavior to avoid the heavy surcharge. Specifically, these owners chose to rent, sell, or personally occupy their vacant units instead of leaving them empty.

Meanwhile, the NYC Comptroller’s office carefully analyzed these behavioral shifts in Vancouver.

The office wanted to account for the high likelihood that local New York owners would modify their behavior in the same way. [Source: New York City Comptroller]

Finally, the office integrated Vancouver’s data into its own financial models to project future tax revenues accurately.

If enough property owners change behavior, actual revenues could fall short of the $500 million projection.

Read Also: Understanding Where Is Your Amended Return: A Guide To Tracking Your 1040-X

Key Legal and Implementation Challenges

From what I have analyzed, here are some of the legal challenges that might surface:

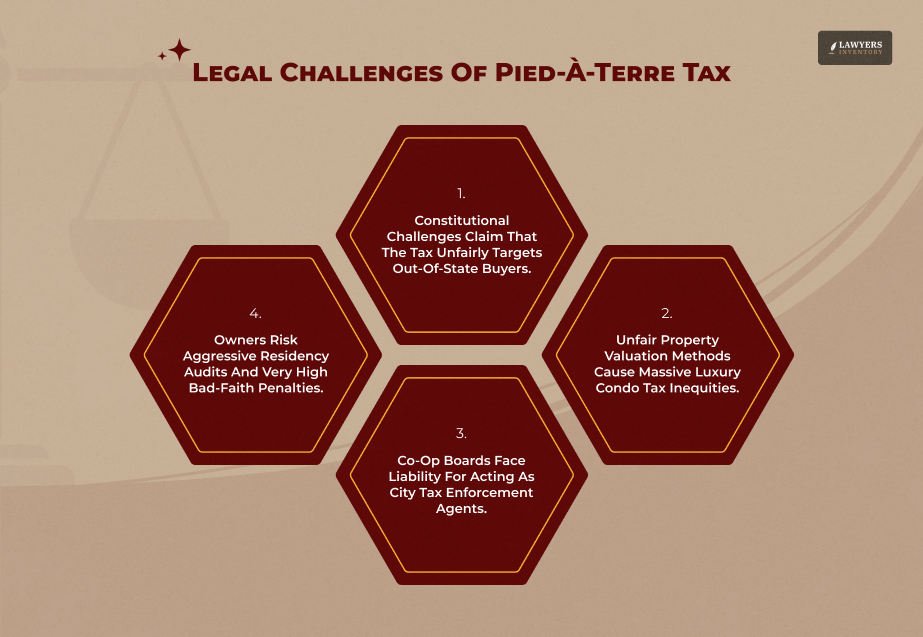

The LLC and Trust Question

The law’s treatment of properties held in LLCs, S-corps, or trusts is one of the significant open questions. Implementation guidance from the DOF will clarify how beneficial ownership is attributed. [Source: Steptoe]

Many high-value NYC properties are held through entities for privacy or estate planning purposes. Until guidance is issued, exposure for entity-held properties remains uncertain.

The Co-Op Collection Mechanism

As per the reports from Cole Schotz, co-op boards are now tasked with collecting the tax from tenant-shareholders. This is an administrative burden that has historically stalled similar proposals.

The co-op collection challenge that has killed pied-à-terre tax bills in committee every year since 2019 has not been fully resolved in the current legislation.

Constitutional Questions

Legal challenges to the surcharge are widely anticipated.

There is an unresolved constitutional question regarding the differential treatment of property owners based on residency status, which plaintiffs could argue violates equal protection principles.

How courts respond to these challenges will significantly shape the tax’s long-term durability.

Deductibility

The pied-à-terre tax is almost certainly not deductible.

New York State does not allow state and local property tax deductions on the state return, and the federal SALT cap further limits federal deductibility. [Source: Reed Corporation]

This increases the effective cost of the surcharge beyond its face rate for most affected owners.

What Options Do Affected Property Owners Have?

Property owners subject to the surcharge have several paths to consider before the January 1, 2027, first payment date:

- Establish primary residence in NYC: This eliminates the surcharge but triggers full NYC personal income tax liability – a significant trade-off for non-residents.

- Rent the property: If the property is rented on a qualifying basis, it may be excluded from the surcharge. Owners should verify the specific rental thresholds with a qualified attorney or CPA.

- Sell: Owners for whom the carrying cost no longer justifies ownership may choose to exit the market entirely.

- Gift or transfer: A parent who gives the apartment to an adult child uses lifetime gift-tax exemption. If the child uses the apartment as a primary residence and pays NYC personal income tax as a resident, the pied-à-terre tax does not apply. This strategy requires careful structuring to withstand DOF scrutiny.

- Wait and contest: Owners who believe they have been incorrectly classified have until after the August 30, 2026 notice date to submit primary residence documentation and contest the determination.

Sources

- New York State FY2026-2027 Enacted Budget – budget.ny.gov

- Assemb. Bill A10009C, 2025-2026 Leg., Reg. Sess. (N.Y. 2026)

- NYC Comptroller’s Fiscal Note – The Pied-à-Terre Tax and Its Potential Revenues (April 30, 2026) – comptroller.nyc.gov

- Steptoe LLP – NYC Pied-à-Terre Tax Effective July 1, 2026 (June 2026)

- Dechert LLP – New York City Imposes Pied-à-Terre Tax (June 2026)

- Cole Schotz P.C. – The New Price of Luxury (June 2026)

- EisnerAmper – NYC Pied-à-Terre Tax Enacted in State Budget (June 2026)

Leave A Reply

Lakeview Data Breach Settlement: Current Status And How To Claim?

Read More

What Is The SALT Tax Deduction And How To Claim It?

Read More

USAA Late Fee Class Action Settlement: $5M Payout And Eligibility Guide

Read More

Aseltine V. BANA Class Settlement – A $21M Bank Fee Victory

Read More

Is WithU Loans Legal And Legit? Legitimacy, Interest Rates, And Risks

Read More

0 Reply

No comments yet.