An aleatory contract, which forms a type of legal agreement, is defined by the fact that the completion of the contract rests entirely upon an event in the future that is uncertain.

With the constantly changing field of law in 2026, such contracts have become very common in the world of insurance and finance.

Presently, there’s quite a bit of ongoing litigation in the United States about how such “risk contracts” are treated by the courts during times of crisis.

If the event in question is vague, it may result in years of litigation. The inequality in value involved makes knowledge about such contracts extremely important.

In this article, we will elaborate on the following:

- The core legal definition and mechanics of an aleatory contract.

- How insurance companies utilize these agreements to manage risk.

- Federal and state legal frameworks that regulate contingent performance.

- Significant US case laws and the “Bad Faith” doctrines of 2026.

- Answers to common questions regarding aleatory rights and obligations.

Defining The Concept Of An Aleatory Contract

What is the Aleatory Contract definition?

An aleatory contract is a legal agreement where the duties of the parties involved are based on a random occurrence.

It differs from a “commutative” contract, where both parties trade things of equal worth instantaneously.

The Key Features of an Aleatory Contract

Understanding what an aleatory contract is requires examining its element of uncertainty.

One of the parties pays a definite sum, whereas the other guarantees a significant reward should a certain calamity or situation arise (Investopedia).

The Importance Of Asymmetrical Value Exchange

The definition of an aleatory contract shows that there is no attempt to balance the “consideration” or value exchanged between the two parties.

An individual might contribute premium payments for thirty years without ever gaining anything, while another might contribute just for a single month yet gain a million dollars in return.

The Role Of Aleatory Contracts In The Insurance Industry

Probably, the primary practical example of this concept is in the field of insurance. An aleatory contract makes it possible for insurance agencies to distribute their risk among numerous clients.

Aleatory Contracts And Risk Management Through Luck

Through such a contract, a person can exchange a relatively minor and certain loss with a larger but uncertain one. This concept constitutes the basis of the American insurance system.

Features Of Aleatory Contract Life Insurance Payouts

The main peculiarity of this type of insurance lies in the fact that in case of aleatory contract life insurance, the “uncertain event” is the time of payment rather than the act of death. The insurer definitely will have to pay, yet the term remains unclear.

What Is An Aleatory Contract In Insurance?

Often people wonder about the meaning of this term in relation to insurance. In order to get a clear answer, you’ll have to know about “adhesion”.

This means that as insurance contracts are aleatory ones, the court will tend to make decisions in favor of the client.

Federal And State Law On Contingent Performance

Some federal laws, such as ERISA, will govern how the aleatory contract is managed concerning the benefits provided to the employees. By 2026, the state supreme court will fine-tune the “Safe Harbor” guidelines for insurance policies.

The Effect Of State Insurance Laws

Several states, including Ohio and Indiana, have issued decisions that when an insurance firm acts in good faith in the case of uncertainty, then they cannot face any “Bad Faith” lawsuit.

Such decisions will keep the aleatory contract system safe from becoming a victim of excessive litigation.

Federal Law And Regulation Supervision

The Federal Government will keep an eye on the solvency of the firms that offer the aleatory contract.

They will ensure that they are financially capable of fulfilling their part of the agreement when the “chance” incident occurs.

Good Faith Is Mandatory

Since the aleatory contract involves uncertainty, the law demands “Utmost Good Faith” from both parties.

The policyholder will be held liable for concealing any necessary information from the insurer.

The latter will then be authorized to cancel the aleatory contract due to the wrong assessment of risk.

The Doctrine Of Utmost Good Faith In Aleatory Agreements

As such, because of the need for parties to be honest as far as any unseen danger associated with the contract is concerned, there is the requirement of a higher level of disclosures.

This concept, commonly referred to as “Uberrimae Fidei,” allows for the accurate calculation of “the chance” being taken by the insurer.

Legal Consequences Of Material Misrepresentations

If, at all, there is material misrepresentation, where one party lies regarding something that may change the terms of the aleatory contract, then the other party has the legal right to refuse payment in case there was indeed a loss.

What this means is that the party whose lie had nothing to do with the loss may still have his/her claims denied.

Fraud Or Concealment?

Concealment entails hiding something about yourself, whereas fraud is actually telling a lie.

Both ruin you in regard to an aleatory contract, but fraud usually comes with additional consequences and bars any refund of any premiums paid out.

Underwriter’s Rescission Rights

In essence, rescission is the cancellation of the aleatory contract. Come 2026, many states will allow an insurer to rescind an insurance contract within a certain “contestability period.”

Distinguishing Aleatory Agreements From Wagering Contracts

There is a very thin dividing line between a legal aleatory contract and an illegal gambling agreement in the US. The most important factor here would be whether the two parties are trying to manage some existing risk or are just creating one to gain money.

Insurable Interest Requirement

In order to make an aleatory contract legal, the one who buys the protection has to have an “insurable interest” in the object being insured against.

You should lose money or emotionally if the “uncertain event” takes place, so that people cannot bet on other persons’ misfortunes.

The Historical Background Of Anti-Gambling Laws

The US courts at early stages did not rely on English common law that sanctioned “life-betting”.

It was decided that any aleatory agreement had to serve society’s good, such as keeping one’s family house or running the business.

The Modern Exceptions In Derivative Market

Derivative instruments like credit default swaps resemble aleatory contracts in many respects in 2026, yet exist in a grey zone of the market. Any activity in these markets is constantly monitored to avoid any gambling system.

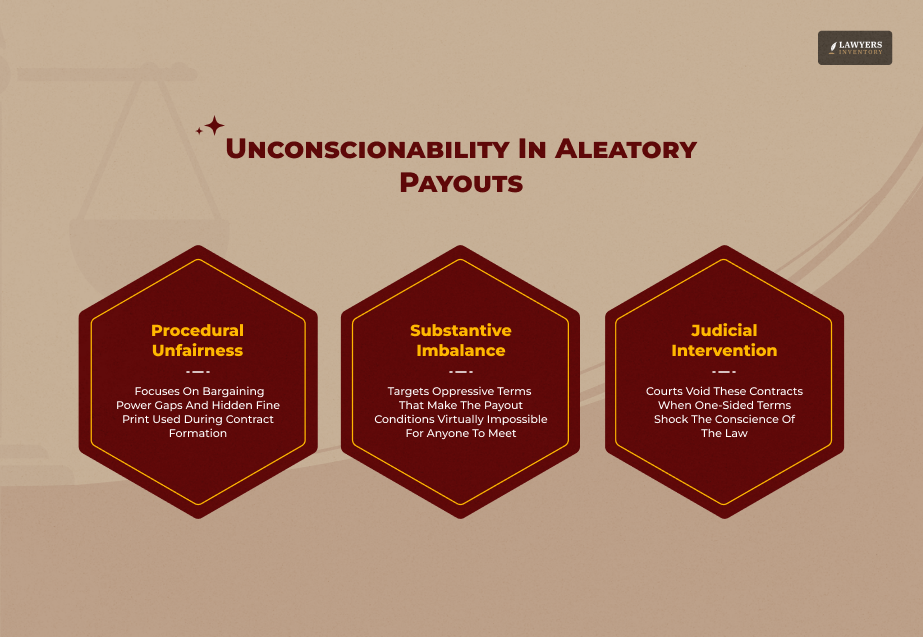

The Concept Of Unconscionability In Aleatory Payouts

The judiciary may intervene when the “unequal exchange” that occurs in the aleatory contract turns predatory or simply too outrageous.

Even while recognizing that exchanges cannot be of equal value, law does not tolerate either side taking advantage of its dominant position to make the other side “lose no matter what”.

Communitive Vs. Aleatory – A Comparative Study

It can be useful to compare the concept of the aleatory contract to the “communitive” nature of ordinary contracts that govern most commercial dealings on a day-to-day basis (e.g., the sale of a new car or the purchase of bread).

When A Standard Contract Transforms Into An Aleatory One

In some cases, a simple commercial contract may become an aleatory contract with the aid of “contingency clauses.”

In this case, a building agreement promising a huge bonus for the condition of favorable weather becomes an aleatory contract.

“If-Then” Bonuses Of Performance Becoming Aleatory Contracts

In the future 2026 gig economy, the employment contracts with “if-then” bonuses will resemble aleatory contracts.

In this case, because of the unpredictable market conditions beyond the control of the employee, performance becomes a matter of chance.

Contemporary Court Rulings On Verdicts

The creation of the law of contingency involves significant court decisions, which lead to the establishment of practices for handling an aleatory contract.

The knowledge of precedents that make it either possible or impossible to make a claim is crucial for a lawyer dealing with such cases.

U.S. Acute Care Sols. v. Drs. Co. Risk Retention Grp. (2025)

This court decision determined that arbitration clauses in an aleatory contract can be considered valid most of the time.

Although you may find that your “risk event” was unjustly handled, there is nothing else you can do about it but resolve matters through an arbitration process.

Frequently Asked Questions (FAQs):

The technical terms of an aleatory contract may seem daunting to most people. Below are answers to the most common issues that citizens encounter when trying to ensure that they are protected by a contingent contract.

Though both are associated with risks, an aleatory contract within an insurance policy serves to mitigate an existing risk.

Gambling involves creating a new risk for financial gain, which is the reason behind gambling being illegal in some instances and insurance being legal.

An aleatory contract may be terminated anytime, although your previous premium payments will not be returned.

After all, the insurance company earned its share since it provided you with insurance for as long as the contract was valid.

If one enters into an aleatory contract despite the fact that the uncertain event is certain, then the contract is null and void. It is fraudulent because the “element of chance” is lacking.

These are take-it-or-leave-it agreements wherein the consumer does not have the authority to negotiate the terms of the contract.

Thus, when there is ambiguity in the contract’s wording, courts tend to give favorable interpretations to those who did not draft it.

Yes, since the amount payable is based on the uncertain discovery of minerals or petroleum. The agreement will result in losses for one of the parties in case no minerals exist within the property.

Yes, warranties of service or products and other “guarantees” fall under this category. For instance, a company promises to repair the product in case it becomes defective, which is an uncertain event.

Any aleatory contract involving insurance or substantial financial benefits must be documented in most states. It avoids confusion regarding the triggering event and the premium price.

Leave A Reply

Hung Jury vs. Mistrial: What Is The Difference And Why It Matters

Read More

NarodniyDimUkraina: An Overview Of The Kyiv-Based Brand Preserving Ukrainian Craftsmanship

Read More

What Is A Mistrial? Legal Definition, Causes, And What Happens Next

Read More

What Is A Sequestered Jury? Legal Definition, Process, And Everything You Need To Know

Read More

What Is A Hung Jury? Legal Definition, Causes, And What Happens Next

Read More

0 Reply

No comments yet.