Today’s topic: MODT

It is very likely that you have come across the term MODT charges if you are going to get a home loan in the near future. Nevertheless, in case you are a completely new borrower, you might not even have a clue what it is.

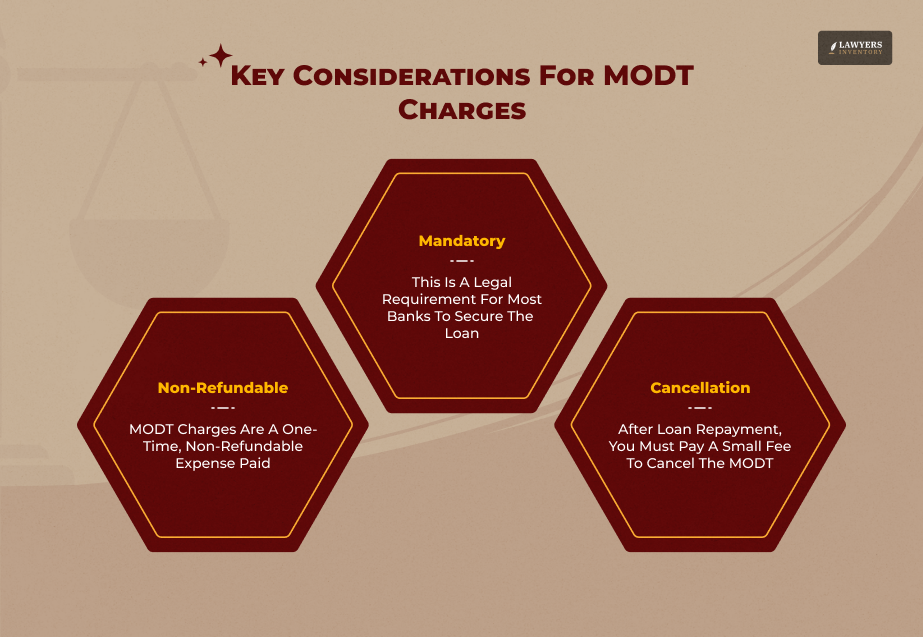

MODT stands for Memorandum for Deposit of Title Deed. This is a compulsory fee imposed on all home loan borrowers.

Essentially, it is a letter of commitment from the borrowers’ side to place the title documents with the authorized lender. In most cases, you are required to hand over this charge to the State Government along with one copy of the loan agreement.

What Is MODT?

As you already know all home loaners need to give the MODT charges. There are some facts about it that you also need to ponder. Even if you think, “What is memorandum title?” it can give you the answer.

The MODT is a non-negotiable charge. As it is a loan fee, the ATLAS (RMW Registration and Title System) enforces it on every home loan borrower.

It is a type of memorandum of title with a specific due date. Every home loan borrower has to give a Memorandum and other home loan processing fees to get a final loan sanction.

If you are taking a loan anytime soon, make sure to apply for the charge described above within a month of mortgaging the house.

Moreover, MODT undertakes the aspect of the loaner’s consent. As a result, the process becomes completely transparent.

Additionally, the legal documents contain a note that the property owner has deposited all title documents to the bank of their own free will. Moreover, the bank has given them a loan amount.

Furthermore, some banks in the country charge extra amounts on the Memorandum. You can consider it as an add-on to the loan processing fee.

This is a stamp duty that the State Government levies against the registration. To your knowledge, the charges of the stamp duty range between 0.1%and 0.2% depending on the total loan amount.

Finally, you should also know that no MODT is mandatory in all states. Generally, the bigger state charges these processing fees for mortgage loans.

MODT Filing Procedure

Now that you know all the vital facts, it is time to go through the filing procedure. Well, there are two ways to file a processing fee for a home loan.

Firstly, the modern e-filing procedure, and secondly, the traditional method. Here, you can go through both procedures stepwise. Have a look:

1. Offline Method

The steps of MODT filing in the traditional way are as follows. Nevertheless, you must remember that this is a temporary method that the government has started for the convenience of the loaners.

(a) Visit the sub-registrars office and bring the MODT notice.

(b) Fill it and drop it again at the sub-registrar’s office.

(c) Make sure the notice contains the details about the property owner.

(d) Expect the government personnel to accept the file within a few working days.

(e) Pay the charges like stamp duty to the government personnel only.

2. Online Method (Also Known As E-Filing Method)

Nowadays, most home loan borrowers choose the MODT e-filing method due to its convenience. It can save time for the loaners and restrict them from moving about much with vital property and bank documents. Check the stepwise procedure here:

(a) Visit the online portal of the Department of Registration and Stamps

(b) Search for all the e-files that are necessary for a MODT application

(c) The place of filing the MODT notice remains the same, that is, the sub-registrars office.

(d) Pay the charges to the government with the help of the Government Receipt Accounting System (GRAS)

Suggest: 10 Reasons Why Businesses Should Hire Corporate Lawyers

Benefits of MODT

If you are a home loan borrower or might turn into one soon, you need to know the benefits of the Memorandum charges. The points are given below:

- MODT allows the loaners to secure the title deed after they make payments.

- The amount of Stamp Duty is always low compared to the loan amount.

- With the presence of MODT, you would need no registration during the property handover.

MODT: Cancellation Process

Now that you know about a couple of MODT application processes, it is time to go through the cancellation process.

According to Tata Capital, the cancellation of MODT is extremely important as “it officially removes the lender’s charge from your property.” They also mention that if you do not complete this step properly, the property will be “legally encumbered.” As a result, this can create problems during important times like:

- Resale.

- Refinancing.

- Legal verification.

In order to resolve this, borrowers should present the following things to the lender:

- The NOC of the lender.

- Original deposit of the title deeds documents.

Additionally, they should also make the payment for the MODT cancellation charges at the sub-registrar’s office.

It is a good habit to consider the MOD in the home loan closure as the last and compulsory step that results in the full restoration of ownership and thus your property records remain clean and free from any kind of disputes.

How To Cancel MODT?

Here are a few steps that you need to take if you are planning to cancel your MODT:

- Cancellation of MODT demands a NOC from the bank’s end. It should contain all the details about the loan. It includes the loan account number, address of the property, and, all identification details of the loaner. Therefore, if you have a home loan, you can only cancel the MODT if the NOC states that the bank has recovered the entire loan amount. Moreover, it does not have any claim on the loaner’s property.

- To cancel your Memorandum, you need to tell your lender for a ‘Deed of Receipt’ and cancel the MODT.

- Visit the sub-registrars office and request him to remove the lien from the property.

Does Pre-Closing A Home Loan Affect MODT?

Pre-closing a home loan (also referred to as a foreclosure) is the step where you completely pay off your remaining loan balance with a single lump-sum payment ahead of the official loan tenure.

On pre-closing a home loan, the property title that was used as collateral for the loan is modified by either removing a lien or canceling the process. This is legally freeing the property from the lender’s charge.

The MODT is a legal instrument that records a charge or lien on your property, benefiting the lender as security for the home loan. In the event of pre-closing (full repayment) of your home loan, this charge is canceled through a formal procedural process.

- Loan Closure and NOC: After the complete repayment of the loan amount, inclusive of any outstanding interest and pre-closure charges, the lender issues the “No Objection Certificate” (NOC) or a loan closure statement. This is an official document confirming that all dues have been cleared.

- Deed of Receipt: The lender also drafts and issues a ‘Deed of Receipt’, which serves as a confirmation that they have received all payments and have revoked the MODT on their side.

- Removal of Lien: The borrower is required to bring these documents (NOC and Deed of Receipt) to the local Sub-Registrar’s office where the original MODT was registered.

- Official Cancellation: The Sub-Registrar’s office cancels the MODT entry in their records and updates the property records to show that the property is no longer charged with any debt or encumbrance.

Who Can Help You With Your MODT?

MODT (Memorandum for Deposit of Title Deed) is a legal document related to property transactions, specifically home loans.

If you need assistance with a MODT, you’ll require a lawyer who specializes in property law, real estate law, or conveyancing.

A property lawyer or conveyancing lawyer can help you with your MODT by:

- Reviewing and drafting the MODT document

- Ensuring compliance with relevant laws and regulations

- Verifying the title deed and property ownership

- Negotiating with lenders or financial institutions

- Resolving any disputes or issues related to the MODT

- Providing guidance on your rights and obligations as a borrower

Furthermore, property lawyers who focus on dealing with MODT will help you with navigating the complexities related to MODT and help you create it easily.

Additionally, they will also ensure that the deed protects your interest and makes the document legally binding.

Read Also: Warranty Deed Vs Quit Claim Deed – Where To Use It?

What Are The MODT Charges?

“MODT charges” are the expenses that are related to the registration of the mortgage or loan, and which normally comprise:

- Stamp Duty: It is a tax levied by the state government and is mostly calculated as a percentage of the loan amount (e.g., 0.1% to 0.5%). However, quite a few states set a limit for the maximum amount.

- Registration Fees: The money given to the Sub-Registrar’s office for the official recording of the lien on the property.

These are the required charges that form part of the home loan program and are almost certainly of the non-refundable type. After the full repayment of the loan, the borrower is obliged to see to it that the MODT is properly canceled and that a “Deed of Receipt” is issued to release the property from the bank’s lien.

Understand Your Rights In MODT

If you are about to take a home loan, do your homework extensively. Remember that the loan process on any non-movable property is tricky. Moreover, there are several home loan processing fees in India.

Besides, when it comes to MODT, you can easily fund it by taking the online approach. However, download all receipts and keep them safe as the loan tenure continues.

This is the way you can avoid a scam. Yet, you need to keep in mind taking legal support while dealing with a bank.

This can keep you away from all types of legal harassment. So, the only thing you would need to do is timely pay the EMIs.

Additionally, the tenure of home loans is generally long, so you need to be very patient. Nevertheless, with proper money management, you can avoid all drawbacks.

More Resources:

Leave A Reply

Understanding What Does Under Contract Mean In Real Estate

Read More

Texas Built Construction Lawsuit Explained: Rights, Remedies, And Legal Truths

Read More

Understanding The Lady Bird Deed: What Is It & How Is It Better?

Read More

Is Section 8 Getting Cut Off: Answering The Most Asked!

Read More

0 Reply

No comments yet.